Dairy Packaging Market Industry Analysis and Forecast 2026-2034

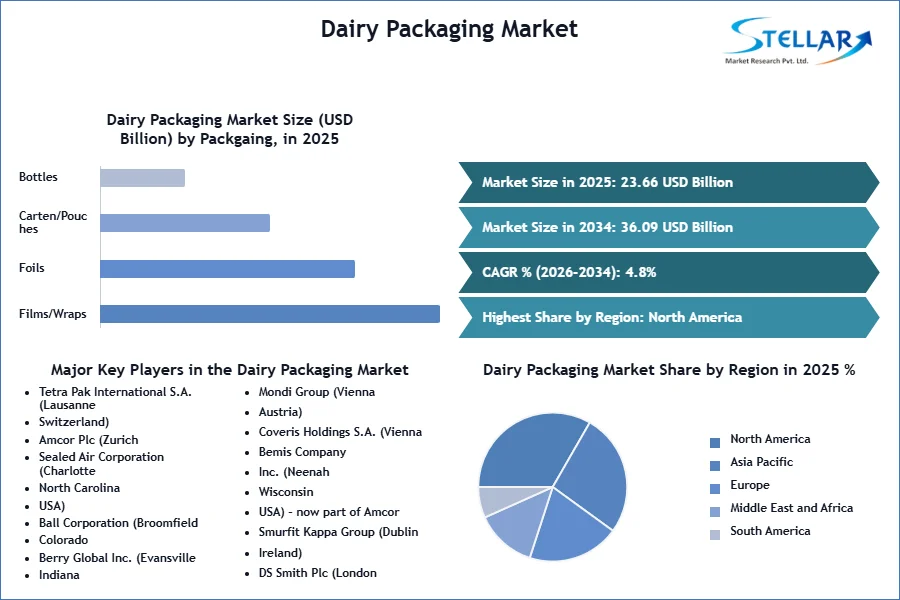

The Dairy Packaging Market size was valued at USD 23.66 Bn. in 2025 and the total Global Dairy Packaging revenue is expected to grow at a CAGR of 4.8% from 2026 to 2034, reaching nearly USD 36.09 Bn. by 2034.

Dairy Packaging Market Overview

The Dairy Packaging Market involves the use of various materials such as plastic, paperboard, glass, and metal to protect and preserve dairy products like milk, cheese, yogurt, butter, and cream. It aims to maintain product freshness and safety, prevent contamination, and extend shelf life while offering convenience to consumers. Common packaging formats include cartons, bottles, tubs, and wrappers, each designed with features like barrier properties, sealing systems, and tamper evidence. Increasingly, sustainability is a focus, with efforts toward using recyclable and biodegradable materials and reducing packaging waste.

Additionally, packaging serves as a vehicle for branding, marketing, and providing essential nutritional information to consumers. The research methodology employed in studying the Dairy Packaging Market typically involves a combination of qualitative and quantitative approaches. Qualitative research includes comprehensive literature reviews, interviews with industry experts, and industry reports and publications analysis to understand market trends, dynamics, and challenges.

Quantitative research involves gathering and analyzing numerical data related to market size, growth rates, revenue, and other relevant metrics. This includes surveys, data mining, and statistical analysis of market data from reputable sources such as industry associations, government agencies, and market research firms. By combining these methodologies, researchers comprehensively understand the Dairy Packaging Market, including its size, growth drivers, competitive landscape, and future outlook. This enables stakeholders to make informed decisions regarding investments, product development, marketing strategies, and more within the paper products industry.

To get more Insights: Request Free Sample Report

Dairy Packaging Market Dynamics

The demand for durable, lightweight, and cost-effective packaging solutions across various industries, including food and beverage, healthcare, personal care, and consumer goods driving the dairy packaging market.

The dairy packaging market is driven by the rising global consumption of dairy products, fueled by population growth, urbanization, and increased awareness of the nutritional benefits of dairy. Health and wellness trends also contribute significantly, as consumers show a preference for natural, organic, and health-enhancing dairy products, necessitating specialized packaging that maintains product integrity. Additionally, the demand for convenience in packaging formats, such as single-serve and easy-to-use options, is increasing due to busy lifestyles. Advances in packaging technology that extend the shelf life of dairy products, reduce food waste and enhance supply chain efficiency further drive the market.

The Dairy Packaging Market includes the development of sustainable packaging solutions, as environmental concerns prompt innovation in recyclable, biodegradable, and eco-friendly materials boosting the opportunities in the dairy packaging market. Technological advancements offer additional opportunities, with smart packaging solutions like sensors that monitor freshness and temperature enhancing product safety and consumer trust. Emerging markets, particularly in developing countries, present new growth prospects for dairy packaging companies. The premiumization trend, where consumers seek out high-quality, artisanal dairy products, also creates opportunities for distinctive packaging that differentiates brands.

The Dairy Packaging Market has a trend for Dairy product packaging sustainability, with a shift towards using sustainable materials and practices to reduce plastic use and increase recyclability. Innovative packaging designs that enhance user experience, such as resealable packs, easy-pour spouts, and portion-controlled sizes, are becoming increasingly popular. The incorporation of smart packaging technology, including QR codes, NFC tags, and freshness indicators, provides consumers with information about product quality and provenance. Minimalist packaging designs that convey transparency and trust align with consumer preferences for natural and less processed foods. Customization and personalization of packaging, catering to individual consumer preferences, are also trending, enhancing brand loyalty and consumer engagement.

Dairy Packaging Market Regional Analysis

In North America, the dairy products packaging market is robust, driven by the high consumption of dairy products and a well-developed dairy industry. The region's dairy packaging market is characterized by a strong emphasis on innovation, sustainability, and consumer convenience. The United States has one of the highest per capita consumption rates of dairy products, including milk, cheese, yogurt, and ice cream, necessitating efficient and effective packaging solutions. Since 2000, the overall per capita consumption of dairy has increased in the U.S. In 2021, consumption was at about 661 pounds per person. As of 2022, consumption had decreased by about eight pounds per person.

Growing consumer awareness of health and wellness leads to increased demand for dairy products perceived as natural and nutritious, requiring packaging that preserves these qualities. There is a significant push towards sustainable packaging solutions, with opportunities for innovation in biodegradable, recyclable, and reduced plastic packaging materials. Consumers and regulatory bodies increasingly demand eco-friendly options. Smart packaging technologies that enhance product safety and consumer engagement, such as QR codes for traceability and freshness indicators, are gaining traction.

Targeting niche markets such as organic, lactose-free, and plant-based dairy alternatives presents opportunities for specialized packaging solutions that cater to these growing segments. The regulatory environment in North America is stringent, with agencies like the FDA (Food and Drug Administration) in the United States and Health Canada ensuring that packaging materials are safe for food contact and that labeling provides accurate nutritional information. These regulations drive the adoption of high-quality, compliant packaging solutions.

Growth in Demand for Dairy Products in China. Meanwhile, the per capita consumption of dairy rose from 36.1 kg per person in 2016 to 42 kg per person in 2023, per data from the Ministry of Agriculture and Rural Affairs (MARA).

Dairy Packaging Market Segment Analysis

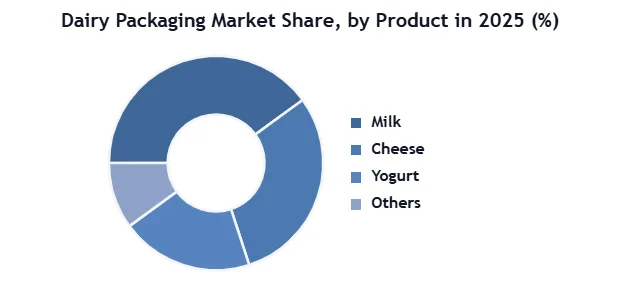

In the dairy packaging market, segmentation by product includes milk, cheese, yogurt, and others. Milk packaging dominates this segment due to the high consumption rates of milk across North America. The demand for convenient and sustainable milk packaging options, such as cartons and plastic jugs, drives this subsegment. Cheese packaging also represents a significant share, driven by the popularity of both processed and artisanal cheeses. Yogurt packaging, with its need for portion control and on-the-go formats, is another crucial subsegment, while others encompass a variety of dairy products such as butter and cream.

By packaging type, bottles are the dominant subsegment in the dairy packaging market. Bottles are widely used for milk and other liquid dairy products due to their convenience and ease of use. Cartons and pouches are also significant, particularly for milk and yogurt, due to their lightweight and sustainable properties. Films/wraps and foils are primarily used for cheese packaging, providing protection and extending shelf life. Tins are less common but are used for specific products like condensed milk. The other category includes innovative packaging solutions like flexible pouches for cream and specialty dairy items.

Plastic is the dominant material in the dairy packaging market, widely used for bottles, tubs, and wraps due to its versatility, durability, and cost-effectiveness. However, there is a growing trend towards more sustainable materials. Paper and paperboard are increasingly popular, especially for milk cartons and yogurt containers, driven by their recyclability and consumer preference for eco-friendly options. Glass, while less common, is favored for premium products due to its reusability and perceived quality. Metal is used primarily for products requiring a long shelf life, such as evaporated and condensed milk. The other materials category includes biodegradable and compostable materials that are gaining traction as sustainability becomes a priority in the industry.

|

Dairy Packaging Market Scope |

|

|

Market Size in 2025 |

USD 23.66 Bn. |

|

Market Size in 2034 |

USD 36.09 Bn. |

|

CAGR (2026-2034) |

4.8% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Segments |

By Product

|

|

By Packaging Type

|

|

|

By Material

|

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Russia, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Key Players in the Dairy Packaging Market

- Tetra Pak International S.A. (Lausanne, Switzerland)

- Amcor Plc (Zurich, Switzerland)

- Sealed Air Corporation (Charlotte, North Carolina, USA)

- Ball Corporation (Broomfield, Colorado, USA)

- Berry Global Inc. (Evansville, Indiana, USA)

- Mondi Group (Vienna, Austria)

- Coveris Holdings S.A. (Vienna, Austria)

- Bemis Company, Inc. (Neenah, Wisconsin, USA) – now part of Amcor

- Smurfit Kappa Group (Dublin, Ireland)

- DS Smith Plc (London, United Kingdom)

- Huhtamaki Oyj (Espoo, Finland)

- Constantia Flexibles Group GmbH (Vienna, Austria)

- RPC Group Plc (Rushden, United Kingdom) – now part of Berry Global

- Ardagh Group S.A. (Luxembourg)

- WestRock Company (Atlanta, Georgia, USA)

- Sonoco Products Company (Hartsville, South Carolina, USA)

- LINPAC Packaging Limited (Featherstone, United Kingdom)

- Winpak Ltd. (Winnipeg, Manitoba, Canada)

- Elopak AS (Oslo, Norway)

- SIG Combibloc Group AG (Neuhausen am Rheinfall, Switzerland)

Frequently Asked Questions

Key players include Tetra Pak International S.A., Amcor Plc, Sealed Air Corporation, Ball Corporation, and Berry Global Inc., among others.

Sustainability is a major focus, with increasing demand for recyclable, biodegradable, and eco-friendly packaging solutions.

Packaging materials and labeling must comply with stringent regulations set by agencies like the FDA in the USA and Health Canada, ensuring safety and accurate nutritional information.

Significant growth is observed in North America, particularly in countries like US and Canada, as well as in Europe.

1. Research Methodology

1.1 Research Data

1.1.1. Primary Data

1.1.2. Secondary Data

1.2. Market Size Estimation

1.2.1. Bottom-Up Approach

1.2.2. Top-Down Approach

1.3. Market Breakdown and Data Triangulation

1.4. Research Assumption

2. Dairy Packaging Market: Executive Summary

2.1. Market Overview

2.2. Market Size (2025) and Forecast (2026 – 2034) and Y-O-Y%

2.3. Market Size (USD) and Market Share (%) – By Segments and Regions

3. Global Dairy Packaging Market: Competitive Landscape

3.1. SMR Competition Matrix

3.2. Key Players Benchmarking

3.2.1. Company Name

3.2.2. Headquarter

3.2.3. Business Segment

3.2.4. End-user Segment

3.2.5. Y-O-Y%

3.2.6. Revenue (2025)

3.2.7. Profit Margin

3.2.8. Market Share

3.2.9. Company Locations

3.3. Market Structure

3.3.1. Market Leaders

3.3.2. Market Followers

3.3.3. Emerging Players

3.4. Consolidation of the Market

3.4.1. Strategic Initiatives and Developments

3.4.2. Mergers and Acquisitions

3.4.3. Collaborations and Partnerships

4. Dairy Packaging Market: Dynamics

4.1. Dairy Packaging Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Dairy Packaging Market Drivers

4.3. Dairy Packaging Market Restraints

4.4. Dairy Packaging Market Opportunities

4.5. Dairy Packaging Market Challenges

4.6. PORTER’s Five Forces Analysis

4.6.1. Intensity of the Rivalry

4.6.2. Threat of New Entrants

4.6.3. Bargaining Power of Suppliers

4.6.4. Bargaining Power of Buyers

4.6.5. Threat of Substitutes

4.7. PESTLE Analysis

4.7.1. Political Factors

4.7.2. Economic Factors

4.7.3. Social Factors

4.7.4. Technological Factor

4.7.5. Legal Factors

4.7.6. Environmental Factors

4.8. Technological Roadmap

4.9. Value Chain Analysis

4.10. Regulatory Landscape

4.10.1. Market Regulation by Region

4.10.1.1. North America

4.10.1.2. Europe

4.10.1.3. Asia Pacific

4.10.1.4. Middle East and Africa

4.10.1.5. South America

4.10.2. Government Schemes and Initiatives

5. Dairy Packaging Market: Global Market Size and Forecast by Segmentation (by Value in USD Million) (2026-2034)

5.1. Dairy Packaging Market Size and Forecast, by Product (2026-2034)

5.1.1. Milk

5.1.2. Cheese

5.1.3. Yogurt

5.1.4. Others

5.2. Dairy Packaging Market Size and Forecast, by Packaging Type (2026-2034)

5.2.1. Films/Wraps

5.2.2. Foils

5.2.3. Carten/Pouches

5.2.4. Bottles

5.2.5. Tins

5.2.6. Others

5.3. Dairy Packaging Market Size and Forecast, by Material (2026-2034)

5.3.1. Glass

5.3.2. Plastic

5.3.3. Paper & Paperboard

5.3.4. Metal

5.3.5. Other

5.4. Dairy Packaging Market Size and Forecast, by Region (2026-2034)

5.4.1. North America

5.4.2. Europe

5.4.3. Asia Pacific

5.4.4. Middle East and Africa

5.4.5. South America

6. North America Dairy Packaging Market Size and Forecast by Segmentation (by Value in USD Million) (2026-2034)

6.1. North America Dairy Packaging Market Size and Forecast, by Product (2026-2034)

6.1.1. Milk

6.1.2. Cheese

6.1.3. Yogurt

6.1.4. Others

6.2. North America Dairy Packaging Market Size and Forecast, by Packaging Type (2026-2034)

6.2.1. Films/Wraps

6.2.2. Foils

6.2.3. Carten/Pouches

6.2.4. Bottles

6.2.5. Tins

6.2.6. Others

6.3. North America Dairy Packaging Market Size and Forecast, by Material (2026-2034)

6.3.1. Glass

6.3.2. Plastic

6.3.3. Paper & Paperboard

6.3.4. Metal

6.3.5. Other

6.4. North America Dairy Packaging Market Size and Forecast, by Country (2026-2034)

6.4.1. United States

6.4.2. Canada

6.4.3. Mexico

7. Europe Dairy Packaging Market Size and Forecast by Segmentation (by Value in USD Million) (2026-2034)

7.1. Europe Dairy Packaging Market Size and Forecast, by Product (2026-2034)

7.2. Europe Dairy Packaging Market Size and Forecast, by Packaging Type (2026-2034)

7.3. Europe Dairy Packaging Market Size and Forecast, by Material (2026-2034)

7.4. Europe Dairy Packaging Market Size and Forecast, by Country (2026-2034)

7.4.1. United Kingdom

7.4.2. France

7.4.3. Germany

7.4.4. Italy

7.4.5. Spain

7.4.6. Sweden

7.4.7. Austria

7.4.8. Rest of Europe

8. Asia Pacific Dairy Packaging Market Size and Forecast by Segmentation (by Value in USD Million) (2026-2034)

8.1. Asia Pacific Dairy Packaging Market Size and Forecast, by Product (2026-2034)

8.2. Asia Pacific Dairy Packaging Market Size and Forecast, by Packaging Type (2026-2034)

8.3. Asia Pacific Dairy Packaging Market Size and Forecast, by Material (2026-2034)

8.4. Asia Pacific Dairy Packaging Market Size and Forecast, by Country (2026-2034)

8.4.1. China

8.4.2. S Korea

8.4.3. Japan

8.4.4. India

8.4.5. Australia

8.4.6. Indonesia

8.4.7. Malaysia

8.4.8. Vietnam

8.4.9. Taiwan

8.4.10. Rest of Asia Pacific

9. Middle East and Africa Dairy Packaging Market Size and Forecast by Segmentation (by Value in USD Million) (2026-2034)

9.1. Middle East and Africa Dairy Packaging Market Size and Forecast, by Product (2026-2034)

9.2. Middle East and Africa Dairy Packaging Market Size and Forecast, by Packaging Type (2026-2034)

9.3. Middle East and Africa Dairy Packaging Market Size and Forecast, by Material (2026-2034)

9.4. Middle East and Africa Dairy Packaging Market Size and Forecast, by Country (2026-2034)

9.4.1. South Africa

9.4.2. GCC

9.4.3. Nigeria

9.4.4. Rest of ME&A

10. South America Dairy Packaging Market Size and Forecast by Segmentation (by Value in USD Million) (2026-2034)

10.1. South America Dairy Packaging Market Size and Forecast, by Product (2026-2034)

10.2. South America Dairy Packaging Market Size and Forecast, by Packaging Type (2026-2034)

10.3. South America Dairy Packaging Market Size and Forecast, by Material (2026-2034)

10.4. South America Dairy Packaging Market Size and Forecast, by Country (2026-2034)

10.4.1. Brazil

10.4.2. Argentina

10.4.3. Rest Of South America

11. Company Profile: Key Players

11.1. Tetra Pak International S.A. (Lausanne, Switzerland)

11.1.1. Company Overview

11.1.2. Business Portfolio

11.1.3. Financial Overview

11.1.3.1. Total Revenue

11.1.3.2. Segment Revenue

11.1.3.3. Regional Revenue

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. Amcor Plc (Zurich, Switzerland)

11.3. Sealed Air Corporation (Charlotte, North Carolina, USA)

11.4. Ball Corporation (Broomfield, Colorado, USA)

11.5. Berry Global Inc. (Evansville, Indiana, USA)

11.6. Mondi Group (Vienna, Austria)

11.7. Coveris Holdings S.A. (Vienna, Austria)

11.8. Bemis Company, Inc. (Neenah, Wisconsin, USA) – now part of Amcor

11.9. Smurfit Kappa Group (Dublin, Ireland)

11.10. DS Smith Plc (London, United Kingdom)

11.11. Huhtamaki Oyj (Espoo, Finland)

11.12. Constantia Flexibles Group GmbH (Vienna, Austria)

11.13. RPC Group Plc (Rushden, United Kingdom) – now part of Berry Global

11.14. Ardagh Group S.A. (Luxembourg)

11.15. WestRock Company (Atlanta, Georgia, USA)

11.16. Sonoco Products Company (Hartsville, South Carolina, USA)

11.17. LINPAC Packaging Limited (Featherstone, United Kingdom)

11.18. Winpak Ltd. (Winnipeg, Manitoba, Canada)

11.19. Elopak AS (Oslo, Norway)

11.20. SIG Combibloc Group AG (Neuhausen am Rheinfall, Switzerland)

12. Key Findings

13. Analyst Recommendations

13.1. Strategic Recommendations

13.2. Future Outlook