Brewers Spent Grain Market Global Industry Analysis and Forecast (2026-2032) by Product, Form, Source and Application

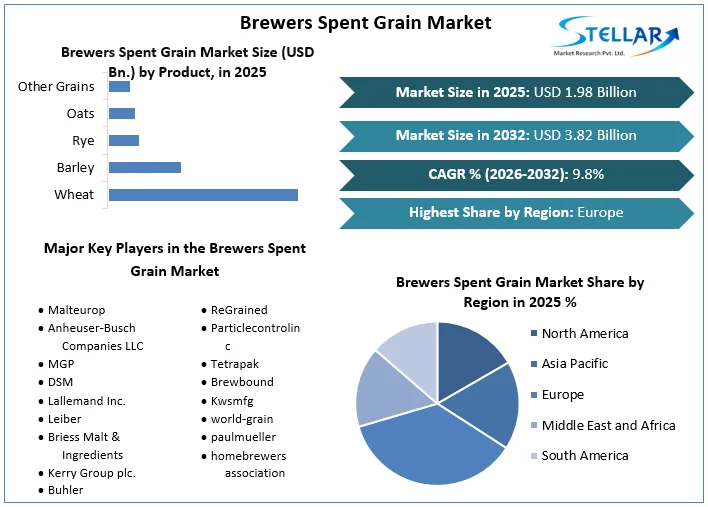

The Brewers Spent Grain Market size was valued at US 1.98 Bn. in 2025 and the total Global Brewer’s Spent grain revenue is expected to grow at a CAGR of 9.8% from 2025 to 2032, reaching nearly USD 3.82 Bn. by 2032.

Brewers Spent Grain Market Overview

The sustainability to focus on various industries is driving the widespread adoption of Brewer’s Spent Grain (BSG) as a renewable resource. With an increasing importance on environmental responsibility, BSG is being utilized across sectors as a sustainable alternative. Additionally, ongoing research and development endeavors are continuously uncovering new applications for BSG, ranging from biofuel production to food fortification and biopolymer synthesis. The innovation in applications is increasing the scope of BSG utilization, contributing to its growing prominence in multiple industries. The BSG market is experiencing a significant increase on a global scale, with emerging economies witnessing heightened adoption of BSG-based products.

The market growth is driven by several key drivers. Initially, the rising global consumption of beer is leading to higher production volumes of BSG, driving market growth. Additionally, environmental concerns and regulatory measures are pushing for the adoption of sustainable solutions like BSG. Finally, technological advancements in BSG processing are enhancing efficiency and diversifying the range of BSG-based products available in the market. These market drivers collectively contribute to the growth and diversification of the BSG market, making it a key player in the sustainable solutions landscape.

Increased production of BSG due to the rise in beer consumption worldwide is driving market growth. At the same time, increased environmental awareness and legislative actions are intensifying the demand for sustainable solutions like BSG. In addition, technological developments in BSG processing are increasing productivity and broadening the variety of BSG-based products that are offered. These interrelated elements play a crucial role in driving the BSG market's growth and diversification and satisfying the need for ecologically friendly solutions across a range of sectors.

To get more Insights: Request Free Sample Report

Brewers Spent Grain Market Dynamics

Role of Brewery Development in Rising BSG Supply

The production of Brewer's Spent Grain (BSG), an unavoidable by-product of brewing, is directly correlated with the rise in production. The amount of BSG produced rises proportionately with each liter of beer produced as breweries grow their production. That clear relationship shows how the craft beer trend has a major impact on the availability and production of BSG, supporting the increase and long-term viability of numerous sectors that depend on this important by-product. Brewer's Spent Grain availability is increasing, which is good for the BSG market in several ways.

The rise is being caused by brewery development. Initially, increased supply results in lower BSG costs, which is expected to make it attractive to companies looking to use it in industries like food manufacturing, biofuels, and animal feed. Widely accessible and less expensive BSG draws in new competitors and promotes innovation in the creation and application of new products. Ultimately, BSG provides a useful outlet for brewers looking to reduce their environmental effects, helping to raise a more sustainable brewing sector. The market of Brewer’s Spent Grain (BSG) applications is growing and becoming more diverse because of this convergence of variables.

BSG as a Sustainable Feedstock opportunity for Biofuel Production

BSG contains carbohydrates and sugars that are converted into biofuels such as ethanol through fermentation processes. As the demand for renewable energy sources continues to rise, BSG offers a sustainable feedstock for biofuel production, contributing to the reduction of greenhouse gas emissions. Brewer's spent grain (BSG) is becoming increasingly in demand as the biofuel industry uses it as a result, breweries are setting up effective systems for collecting and processing BSG. Despite it was once thought of as trash, BSG is now a valuable ingredient for the manufacture of biofuel, providing breweries with an additional source of income that could help them with their brewing costs.

The biofuel application attracts new companies and diversifies the use of BSG, hence increasing the market. The diversification demonstrates that BSG is increasingly seen as a valuable resource across a range of industries and not only optimizes BSG utilization but also has the potential to lower overall disposal costs for breweries.

Impact of High Moisture Content on Quality and Shelf Life is challenging

BSG has a high moisture content and is susceptible to spoiling, necessitating suitable storage and preservation measures to ensure its quality. It makes it difficult for breweries and BSG users to control inventory and cut down on waste. BSG's perishable nature complicates logistics, potentially increasing transportation costs and limiting its geographical reach. According to Stellar research its shows that, transportation costs as a significant factor in BSG utilization, further impacted by the need for rapid transport due to its perishability. Efficient storage and preservation solutions are crucial for breweries to manage BSG inventory without spoilage, as inefficiencies lead to waste and reduced revenue streams. Concerns about maintaining quality and preventing waste are expected to deter potential users, posing challenges to market adoption of BSG and its applications.

Drying BSG reduces moisture content, extending shelf life and simplifying storage and transportation. Its energy-intensive nature, however, compromises cost-effectiveness. Anaerobic BSG fermentation through ensiling improves storage stability but necessitates certain tools and expertise. Proximity between breweries and BSG users promotes on-site consumption by enabling the prompt use of fresh BSG and reducing storage issues. The approach underscores the importance of geographic closeness for optimizing the use of BSG and resolving logistical issues related to its maintenance and storage.

Brewers Spent Grain Market Segment Analysis

By Product, Barley, being relatively cheap and widely accessible, makes barley BSG a cost-effective choice for various applications. Its dominance in brewing ensures the highest volume of production among all BSG types, ensuring a consistent and dependable supply. According to SMR Research, in 2025 barley remained the most utilized brewing grain in the United States, with over 60% of all beers brewed using barley. The substantial barley usage results in a significant generation of barley BSG, reinforcing its abundant availability and affordability for users across various industries. With its abundance, barley BSG presents opportunities for large-scale applications such as biofuel production, contributing to a more sustainable energy landscape.

Research published in Fuel Processing Technology in 2025 confirms barley BSG's viability as a feedstock for bioethanol production, with conversion efficiencies comparable to other cellulosic materials. This supports its potential for biofuel applications. Additionally, the availability and affordability of barley BSG attracts new market entrants, particularly in sectors like animal feed and bioplastics, where BSG offers a cost-competitive and sustainable alternative to traditional materials, promoting market growth.

Brewers Spent Grain Market Regional Insights

Europe's significant BSG generation and long history of brewing contribute to its dominance in the worldwide BSG market. According to Stellar Research, Europe's revenue share in 2025 was 34.1%, indicating the region's leading position in the manufacturing and use of BSG. Brazil ranks third globally in beer production, following China and the USA, contributing 5% to the world beer market. The brewing process involves converting starch from barley malt into fermentable wort, which is then boiled with hops, cooled, and fermented with brewer’s yeast. BSG, the major lignocellulosic biomass waste generated in the beer industry, poses economic and environmental challenges regarding its disposal. However, it holds significant potential for various applications, including animal feed, food fortification, biofuel production, and biorefinery processes. The Brazilian beer industry has witnessed exponential growth in recent years, resulting in a rapid increase in registered beer companies.

According to data from the Ministry of Agriculture, Livestock and Food Supply (MAPA) in 2022, the number of registered beer companies in Brazil has surged, especially between 2018 and 2021. The growth trajectory indicates a corresponding increase in BSG generation, raising concerns about its disposal and utilization. The perishable nature of BSG complicates logistics and transportation, potentially increasing costs and limiting its geographical reach. The drying process, although effective in extending shelf life and facilitating storage, is energy-intensive, impacting cost-effectiveness. Ensiling, an alternative preservation method, requires specialized equipment and expertise but offers enhanced storage stability. However, storage and preservation challenges are expected to discourage potential users, hindering market adoption of BSG and its applications.

Europe, particularly countries Including Germany and France, is increasingly prioritizing sustainability in the brewing industry, driving exploration of innovative BSG applications such as biofuel production and incorporation into food products. SMR report highlights ongoing research projects focusing on BSG's potential for bioethanol production and novel food ingredients, indicating Europe's commitment to sustainable BSG utilization.

The EU's Circular Economy Action Plan, with a target for a 50% reduction in food waste by 2032, supports BSG valorization by promoting waste reduction and resource recovery initiatives. Also, strict waste management regulations in countries like Germany incentivize breweries to find responsible outlets for their BSG, while government grants support research on innovative BSG applications. Germany leads BSG production in Europe, producing over 85 million hectoliters of beer in 2021, significantly contributing to the region's BSG generation. The focus on sustainability, coupled with government initiatives and Germany's prominent role in beer production, drives market growth and innovation in BSG utilization in Europe.

Brewers Spent Grain Market Competitive Landscape

Large sums of money are being spent on R&D by both well-established businesses and start-ups to extend the market of BSG-based products by improving processing methods and finding new uses for the material. In addition, larger organizations strategically buy out smaller firms that have access to the market or special BSG processing technologies to strengthen their position as market leaders. Increased competition from new players and innovative products is driving market growth and benefiting consumers with lower prices and a broader range of BSG-based products. Overcoming storage and transportation challenges allows the market to reach new customer segments across industries.

The competitive landscape is also fostering sustainability practices within the brewing industry and beyond, pushing the boundaries of BSG utilization towards more environmentally friendly solutions. The intensified competition drives innovation, promotes market growth, and encourages sustainable practices, ultimately enhancing the overall value proposition of BSG-based products for consumers and industries alike.

- A joint venture called Circular Food Solutions Switzerland AG was established in July 2022 by Bühler, a global provider of process and equipment technologies for the food and beverage, agricultural, and feed sectors, and CN & Partners, an investment firm with headquarters in Switzerland. The goal of the venture is to create a Swiss meat substitute by utilizing recycled spent grain.

- Osage Foods, a Missouri-based supplier of ingredients and ingredient systems, unveiled SolvPro, a new range of vegan plant protein blends, in January 2023. EverPro, an upcycled grain obtained from the brewing business Anheuser-Busch InBev (AB InBev), is used to make these protein blends.

|

Brewers Spent Grain Market Scope |

|

|

Market Size in 2025 |

USD 1.98 Bn. |

|

Market Size in 2032 |

USD 3.82 Bn. |

|

CAGR (2026-2032) |

9.8 % |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segment Scope |

By Product Wheat Barley Rye Oats Other Grains |

|

By Application Animal Feed Cattle (Dairy/Beef) Horse Feed Poultry Food & Beverages Dietary Supplements |

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Key Player in the Brewers Spent Grain Market

- Malteurop

- Anheuser-Busch Companies LLC

- MGP

- DSM

- Lallemand Inc.

- Leiber

- Briess Malt & Ingredients

- Kerry Group plc.

- Buhler

- ReGrained

- Particlecontrolinc

- Tetrapak

- Brewbound

- Kwsmfg

- world-grain

- paulmueller

- homebrewers association

Frequently Asked Questions

Yes, emerging trends in the BSG market include the exploration of innovative applications for BSG, such as biofuel production and incorporation into food products, as well as increasing emphasis on sustainability and circular economy initiatives.

Some challenges associated with BSG utilization include its perishable nature, which requires proper storage and transportation, as well as regulatory compliance regarding its use in food and beverage products.

The Market size was valued at USD 1.98 Billion in 2025 and the total Market revenue is expected to grow at a CAGR of 9.8 % from 2026 to 2032, reaching nearly USD 3.82 Billion.

The segments covered in the market report are By Product and Application.

1. Research Methodology

1.1 Research Data

1.1.1. Primary Data

1.1.2. Secondary Data

1.2. Market Size Estimation

1.2.1. Bottom-Up Approach

1.2.2. Top-Down Approach

1.3. Market Breakdown and Data Triangulation

1.4. Research Assumption

2. Brewers Spent Grain Market Executive Summary

2.1. Market Overview

2.2. Market Size (2025) and Forecast (2026– 2032) and Y-O-Y%

2.3. Market Size (USD) and Market Share (%) – By Segments and Regions

3. Global Brewers Spent Grain Market: Competitive Landscape

3.1. SMR Competition Matrix

3.2. Key Players Benchmarking

3.2.1. Company Name

3.2.2. Headquarter

3.2.3. Product Segment

3.2.4. End-user Segment

3.2.5. Y-O-Y%

3.2.6. Revenue (2025)

3.2.7. Profit Margin

3.2.8. Market Share

3.2.9. Company Locations

3.3. Market Structure

3.3.1. Market Leaders

3.3.2. Market Followers

3.3.3. Emerging Players

3.4. Consolidation of the Market

3.4.1. Strategic Initiatives and Developments

3.4.2. Mergers and Acquisitions

3.4.3. Collaborations and Partnerships

4. Brewers Spent Grain Market: Dynamics

4.1. Brewers Spent Grain Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Brewers Spent Grain Market Drivers

4.3. Brewers Spent Grain Market Restraints

4.4. Brewers Spent Grain Market Opportunities

4.5. Brewers Spent Grain Market Challenges

4.6. PORTER’s Five Forces Analysis

4.6.1. Intensity of the Rivalry

4.6.2. Threat of New Entrants

4.6.3. Bargaining Power of Suppliers

4.6.4. Bargaining Power of Buyers

4.6.5. Threat of Substitutes

4.7. PESTLE Analysis

4.7.1. Political Factors

4.7.2. Economic Factors

4.7.3. Social Factors

4.7.4. Technological Factor

4.7.5. Legal Factors

4.7.6. Environmental Factors

4.8. Technological Roadmap

4.9. Value Chain Analysis

4.10. Regulatory Landscape by Region

4.10.1. North America

4.10.2. Europe

4.10.3. Asia Pacific

4.10.4. Middle East and Africa

4.10.5. South America

5. Brewers Spent Grain Market: Global Market Size and Forecast by Segmentation (by Value in USD Million and Volume in Metric Tons) (2025-2032)

5.1. Brewers Spent Grain Market Size and Forecast, by Product (2025-2032)

5.1.1. Wheat

5.1.2. Barley

5.1.3. Rye

5.1.4. Oats

5.1.5. Other Grains

5.2. Brewers Spent Grain Market Size and Forecast, by Application (2025-2032)

5.2.1. Animal Feed

5.2.2. Cattle (Dairy/Beef)

5.2.3. Horse Feed

5.2.4. Poultry

5.2.5. Food & Beverages

5.2.6. Dietary Supplements

5.3. Brewers Spent Grain Market Size and Forecast, by Region (2025-2032)

5.3.1. North America

5.3.2. Europe

5.3.3. Asia Pacific

5.3.4. Middle East and Africa

5.3.5. South America

6. North America Brewers Spent Grain Market Size and Forecast by Segmentation (by Value in USD Million and Volume in Metric Tons) (2025-2032)

6.1. North America Brewers Spent Grain Market Size and Forecast, by Product (2025-2032)

6.1.1. Wheat

6.1.2. Barley

6.1.3. Rye

6.1.4. Oats

6.1.5. Other Grains

6.2. North America Brewers Spent Grain Market Size and Forecast, by Application (2025-2032)

6.2.1. Animal Feed

6.2.2. Cattle (Dairy/Beef)

6.2.3. Horse Feed

6.2.4. Poultry

6.2.5. Food & Beverages

6.2.6. Dietary Supplements

6.3. North America Brewers Spent Grain Market Size and Forecast, by Country (2025-2032)

6.3.1. United States

6.3.2. Canada

6.3.3. Mexico

7. Europe Brewers Spent Grain Market Size and Forecast by Segmentation (by Value in USD Million and Volume in Metric Tons) (2025-2032)

7.1. Europe Brewers Spent Grain Market Size and Forecast, by Product (2025-2032)

7.2. Europe Brewers Spent Grain Market Size and Forecast, by Application (2025-2032)

7.3. Europe Brewers Spent Grain Market Size and Forecast, by Country (2025-2032)

7.3.1. United Kingdom

7.3.2. France

7.3.3. Germany

7.3.4. Italy

7.3.5. Spain

7.3.6. Sweden

7.3.7. Austria

7.3.8. Rest of Europe

8. Asia Pacific Brewers Spent Grain Market Size and Forecast by Segmentation (by Value in USD Million and Volume in Metric Tons) (2025-2032)

8.1. Asia Pacific Brewers Spent Grain Market Size and Forecast, by Product (2025-2032)

8.2. Asia Pacific Brewers Spent Grain Market Size and Forecast, by Application (2025-2032)

8.3. Asia Pacific Brewers Spent Grain Market Size and Forecast, by Country (2025-2032)

8.3.1. China

8.3.2. S Korea

8.3.3. Japan

8.3.4. India

8.3.5. Australia

8.3.6. Indonesia

8.3.7. Malaysia

8.3.8. Vietnam

8.3.9. Taiwan

8.3.10. Rest of Asia Pacific

9. Middle East and Africa Brewers Spent Grain Market Size and Forecast by Segmentation (by Value in USD Million and Volume in Metric Tons) (2025-2032)

9.1. Middle East and Africa Brewers Spent Grain Market Size and Forecast, by Product (2025-2032)

9.2. Middle East and Africa Brewers Spent Grain Market Size and Forecast, by Application (2025-2032)

9.3. Middle East and Africa Brewers Spent Grain Market Size and Forecast, by Country (2025-2032)

9.3.1. South Africa

9.3.2. GCC

9.3.3. Nigeria

9.3.4. Rest of ME&A

10. South America Brewers Spent Grain Market Size and Forecast by Segmentation (by Value in USD Million and Volume in Metric Tons) (2025-2032)

10.1. South America Brewers Spent Grain Market Size and Forecast, by Product (2025-2032)

10.2. South America Brewers Spent Grain Market Size and Forecast, by Application (2025-2032)

10.3. South America Brewers Spent Grain Market Size and Forecast, by Country (2025-2032)

10.3.1. Brazil

10.3.2. Argentina

10.3.3. Rest Of South America

11. Company Profile: Key Players

11.1. Malteurop

11.1.1. Company Overview

11.1.2. Business Portfolio

11.1.2.1. Product Name

11.1.2.2. Product Details (Price, Features, etc)

11.1.3. Financial Overview

11.1.3.1. Total Revenue

11.1.3.2. Segment Revenue

11.1.3.3. Regional Revenue

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. Anheuser-Busch Companies LLC

11.3. MGP

11.4. DSM

11.5. Lallemand Inc.

11.6. Leiber

11.7. Briess Malt & Ingredients

11.8. Kerry Group plc.

11.9. Buhler

11.10. ReGrained

11.11. Particlecontrolinc

11.12. Tetrapak

11.13. Brewbound

11.14. Kwsmfg

11.15. world-grain

11.16. paulmueller

11.17. homebrewers association

12. Key Findings

13. Analyst Recommendations

13.1. Strategic Recommendations

13.2. Future Outlook