White Coal Market Global Industry Analysis and Forecast (2026-2032)

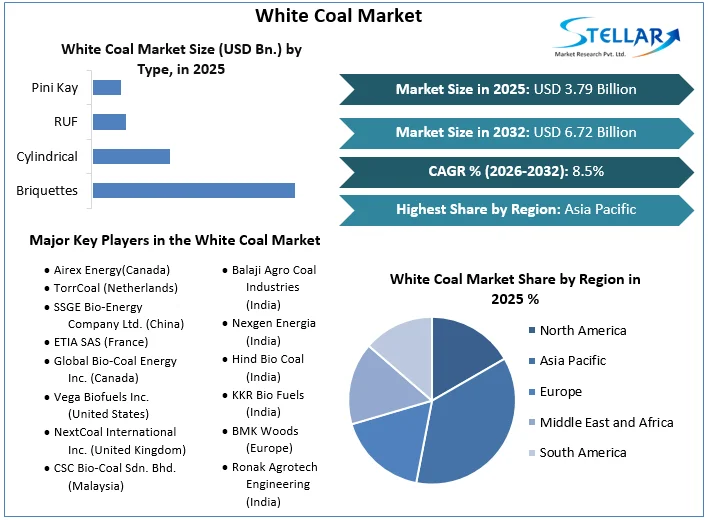

The White Coal Market size was valued at USD 3.79 Bn. in 2025 and the total Global White Coal revenue is expected to grow at a CAGR of 8.5 % from 2026 to 2032, reaching nearly USD 6.72 Bn. by 2032.

White Coal Market Overview

White coal refers to the briquettes or pellets made from biomass materials, such as agricultural waste, sawdust, and wood residues. These materials are compressed under high pressure without the use of any chemical binders, resulting in dense and energy-rich solid fuel.

The comprehensive report by Stellar Market Research provides an in-depth analysis of the White Coal Market with a focus on predicting market growth trends. It offers valuable insights into the dynamics of the value chain and the supply chain. By analyzing the scope of the White Coal market, this report provides a detailed understanding of the complex network of processes and stakeholders that are involved in the production, distribution, and application of these additives. The research objective is to gain a better understanding of the current landscape of usage, applications, and management strategies for this food additive.

The report emphasizes the significance of import and export activities in the White Coal market since they ensure continuous transactions between suppliers and end-users. Key players play a crucial role in driving innovation and improving product efficacy, underscoring the importance of targeted strategies to meet evolving consumer demands. Additionally, the analysis assesses the cost-profit ratio, which enables the evaluation of companies' financial capabilities for investing in research and development aimed at introducing new products or improving existing ones.

The growth and innovation of the market are driven by opportunities in new product development and advancements in formulation technologies. The report offers statistical data on the effectiveness of White Coal in various applications and its impact on market trends through quantitative research methods. Competitive intelligence analysis helps to understand market dynamics, competitor strategies, and customer perceptions, providing market players with a competitive advantage in the global White Coal market.

To get more Insights: Request Free Sample Report

White Coal Market Dynamics

Emergence of White Coal Market in Response to Growing Clean Energy Demands and Depleting Fossil Fuel Resources.

The global white coal market has been significantly impacted by the increasing demand for clean energy and the rapid depletion of fossil fuels. A comprehensive analysis of the value chain indicates that the market growth is being driven by the need for alternative energy sources. White coal, also known as biomass briquettes, has emerged as a viable solution to address concerns regarding environmental degradation and climate change driving the demand for White Coal Market. Companies operating in the market are witnessing a positive trend in profit margins, primarily owing to the growing adoption of eco-friendly energy solutions. The main factor contributing to the growth of the white coal market is the increasing concern over carbon emissions and their negative impact on the environment.

As fossil fuel reserves continue to decline, there is a persistent need to explore renewable energy sources to meet global energy demands sustainably which drives the white coal market. This shift in focus has resulted in a surge of investments in the white coal manufacturing industries, as stakeholders recognize its potential to reduce greenhouse gas emissions while providing a reliable source of energy. A feasibility study of the market reveals promising opportunities for growth and diversification. As governments worldwide implement stringent regulations aimed at reducing carbon footprints, the demand for clean energy solutions continues to rise.

This presents a favorable environment for the growth of the white coal market. The current regulatory environment offers advantageous market conditions for white coal producers to take advantage of emerging opportunities and establish a solid presence in the renewable energy sector. The increasing demand for clean energy, along with the diminishing fossil fuel resources, is driving the growth of the global white coal market.

Challenges in Logistics, Infrastructure, and Cost Competitiveness

The global white coal market faces significant challenges in terms of logistics, infrastructure, and cost competitiveness. These challenges act as restraints, hindering the efficient distribution of white coal products. Inadequate transportation networks and underdeveloped infrastructure in key production regions are major barriers to entry, making it difficult for producers to distribute their products effectively.

The volatility in transportation costs further complicates the situation, making it challenging for producers to maintain competitive pricing strategies. Additionally, reimbursement policies related to renewable energy sources do not provide sufficient incentives for investment in white coal logistics infrastructure, resulting in a lack of reimbursement for transportation and distribution expenses. Trade policies, including tariffs and import/export regulations, impede the smooth flow of white coal across borders, adding complexity to market dynamics. Also, market consolidation within the transportation and logistics sector limits competition, leading to higher costs for white coal transportation and distribution.

White Coal Market Segment Analysis

By Type, According to SMR research, the Briquettes segment is the largest in 2025. It holds about 60% of the market share and dominates the white coal market. Consumers are increasingly preferring briquettes over traditional coal thanks to their higher energy density, lower emissions, and ease of handling. Briquettes are also more environmentally friendly than traditional coal, as they are made from compressed biomass waste, such as sawdust, agricultural waste, and other organic materials. This has led to a growing demand for briquettes, particularly in developing countries where access to electricity is limited, and biomass waste is abundant.

Leading players in the white coal market, such as Airex Energy, TorrCoal, SSGE Bio-Energy Company Ltd., Enviva Biomass Inc., and RWE AG, have recognized the potential of the briquette segment and have invested heavily in branding strategies to promote their products. These companies have focused on marketing their briquettes as a cleaner and more sustainable alternative to traditional coal, highlighting their benefits in terms of energy efficiency, emissions reduction, and waste reduction. The production cost of briquettes is also lower than traditional coal, making them a more cost-effective option for consumers. In terms of imports and exports, briquettes are a popular commodity in the global market.

The supply chain of the briquette segment is also well-established, with several companies involved in the production, distribution, and sales of briquettes. The top-selling region of briquettes is the Asia Pacific region, where demand is driven by the region's large population, growing energy demand, and increasing focus on renewable energy sources. The briquette segment is the dominant segment in the global white coal market, accounting for a significant share of the market. The growth of this segment has been attributed to several factors, including consumer preference, leading players' branding strategies, and production cost efficiency. The briquette segment is expected to continue to grow in the coming years, driven by the increasing demand for cleaner and more sustainable energy sources.

White Coal Market Regional Analysis

Asia Pacific holds a dominant position in the White Coal Market in 2025 with a market share of about XX%. The increasing environmental concerns throughout the region, particularly in nations such as China and India, have sparked a notable transition towards renewable energy sources. White coal, which serves as a cleaner alternative to traditional coal, emerges as a viable solution. The region's abundance of biomass resources acts as a significant catalyst for growth. China, being a prominent agricultural producer, possesses vast quantities of agricultural residues like straw and rice husks, which serve as ideal feedstock for white coal production. Similarly, India's thriving forestry sector generates ample wood waste that’s converted into white coal.

This easy access to raw materials empowers regional production and market penetration, distinguishing it from regions with limited biomass resources. The key companies in the white coal market have established themselves in the Asia Pacific region. They leverage government support and favorable trade policies within the region to expand their market presence. For example, China's supportive policies for biomass energy production incentivize white coal production, creating a more favorable environment compared to regions with stricter regulations. Additionally, the dominance of the Asia Pacific region in the White Coal Market is further solidified by observing market penetration.

China, with its extensive industrial sector, is likely to be the top-selling country in the white coal market. India closely follows, driven by its growing industries and increasing demand for cleaner energy sources. This regional market penetration is evident in the significant economic impact, as the Asia Pacific market is expected to contribute a substantial portion of the global market's revenue. This notable increase in revenue underscores the region's pivotal role in shaping the future of the white coal market. The convergence of environmental concerns, abundant biomass resources, strong government support, and leading companies positions the Asia Pacific region as the unrivaled leader in the white coal market.

White Coal Market Competitive Landscape

The Global White Coal Market industry is competitive among companies owing to the presence of numerous players across the industry. The major players in the market include etc. These companies are pushing boundaries, investing in research and development to expand their product lines, and undertaking strategic activities including new product launches, contractual agreements, mergers and acquisitions, and collaborations with other organizations. The future of the White Coal Market promises to be vibrant and dynamic, driven by the increasing demand for clean and renewable energy sources, along with growing concerns regarding environmental degradation and climate change.

- In 2023, Airex Energy, in collaboration with Groupe Rémabec and SUEZ, unveiled a groundbreaking biochar plant in Port-Cartier, Quebec, with plans to become the largest biochar plant in North America by 2026, producing 350,000 tonnes of biochar by 2035. This initiative aims to sequester carbon, generate carbon credits, and contribute to achieving carbon-neutral targets set by the Paris Agreements.

- In 2023, TorrCoal became a Perpetual Next Company, signaling its commitment to scaling up torrefaction technology as a short-term solution to reduce CO2 emissions.

- In 2023 Vega Biofuels Inc. announced the expansion of its manufacturing capabilities to include multiple sizes of its biocoal product, utilizing its "generation 4 machine" to produce bio-coal resembling traditional Powder River Basin Coal in both powder and pellet forms. This strategic move aims to cater to diverse customer needs and applications, enhancing the company's market reach and product offerings

|

White Coal Market Scope |

|

|

Market Size in 2025 |

USD 3.79 Bn. |

|

Market Size in 2032 |

USD 6.72 Bn. |

|

CAGR (2026-2032) |

8.5 % |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

|

By Type Briquettes Cylindrical RUF Pini Kay Others |

|

|

By Process Torrefaction Pyrolysis Hydrothermal Carbonization Others |

|

|

By End Use Ceramic Power Generation Food & Beverage Textile Industry Others |

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Key Player in the White Coal Market

- Airex Energy(Canada)

- TorrCoal (Netherlands)

- SSGE Bio-Energy Company Ltd. (China)

- ETIA SAS (France)

- Global Bio-Coal Energy Inc. (Canada)

- Vega Biofuels Inc. (United States)

- NextCoal International Inc. (United Kingdom)

- CSC Bio-Coal Sdn. Bhd. (Malaysia)

- Balaji Agro Coal Industries (India)

- Nexgen Energia (India)

- Hind Bio Coal (India)

- KKR Bio Fuels (India)

- BMK Woods (Europe)

- Ronak Agrotech Engineering (India)

- Green Fuel India (India)

Frequently Asked Questions

Growing demand for sustainable energy and the development of new types of white coal are opportunities in the White Coal market.

The Asia Pacific region is expected to dominate the market share throughout the forecasted period, fueled by the presence of major agricultural economies and growing worries about pollution.

The Market size was valued at USD 3.79 Billion in 2025 and the total Market revenue is expected to grow at a CAGR of 8.5 % from 2026 to 2032, reaching nearly USD 6.72 billion.

The segments covered in the market report are Type, process, end use and region.

1. White Coal Market: Research Methodology

2. White Coal Market: Executive Summary

3. White Coal Market: Competitive Landscape

4. Potential Areas for Investment

4.1. Stellar Competition Matrix

4.2. Competitive Landscape

4.3. Key Players Benchmarking

4.4. Market Structure

4.4.1. Market Leaders

4.4.2. Market Followers

4.4.3. Emerging Players

4.5. Consolidation of the Market

4.6. Global Import-Export Analysis

5. White Coal Market: Dynamics

5.1. Market Driver

5.1.1. Demand for clean-label acidity regulators

5.1.2. The use of natural and organic White Coal

5.2. Market Trends by Region

5.2.1. North America

5.2.2. Europe

5.2.3. Asia Pacific

5.2.4. Middle East and Africa

5.2.5. South America

5.3. Market Drivers by Region

5.3.1. North America

5.3.2. Europe

5.3.3. Asia Pacific

5.3.4. Middle East and Africa

5.3.5. South America

5.4. Market Restraints

5.5. Market Opportunities

5.6. Market Challenges

5.7. PORTER’s Five Forces Analysis

5.8. PESTLE Analysis

5.9. Strategies for New Entrants to Penetrate the Market

5.10. Regulatory Landscape by Region

5.10.1. North America

5.10.2. Europe

5.10.3. Asia Pacific

5.10.4. Middle East and Africa

5.10.5. South America

6. White Coal Market Size and Forecast by Segments (by Value Units)

6.1. White Coal Market Size and Forecast, by Product (2025-2032)

6.1.1. Briquettes

6.1.2. Cylindrical

6.1.3. RUF

6.1.4. Pini Kay

6.1.5. Others

6.2. White Coal Market Size and Forecast, by Application (2025-2032)

6.2.1. Torrefaction

6.2.2. Pyrolysis

6.2.3. Hydrothermal Carbonization

6.2.4. Others

6.3. White Coal Market Size and Forecast, by End Use (2025-2032)

6.3.1. Ceramic

6.3.2. Power Generation

6.3.3. Food & Beverage

6.3.4. Textile Industry

6.3.5. Others

6.4. White Coal Market Size and Forecast, by Region (2025-2032)

6.4.1. North America

6.4.2. Europe

6.4.3. Asia Pacific

6.4.4. Middle East and Africa

6.4.5. South America

7. North America White Coal Market Size and Forecast (by Value Units)

7.1. North America White Coal Market Size and Forecast, by Product (2025-2032)

7.1.1. Briquettes

7.1.2. Cylindrical

7.1.3. RUF

7.1.4. Pini Kay

7.1.5. Others

7.2. North America White Coal Market Size and Forecast, by Application (2025-2032)

7.2.1. Torrefaction

7.2.2. Pyrolysis

7.2.3. Hydrothermal Carbonization

7.2.4. Others

7.3. North America White Coal Market Size and Forecast, by End Use (2025-2032)

7.3.1. Ceramic

7.3.2. Power Generation

7.3.3. Food & Beverage

7.3.4. Textile Industry

7.3.5. Others

7.4. North America White Coal Market Size and Forecast, by Country (2025-2032)

7.4.1. United States

7.4.2. Canada

7.4.3. Mexico

8. Europe White Coal Market Size and Forecast (by Value Units)

8.1. Europe White Coal Market Size and Forecast, by Product (2025-2032)

8.1.1. Briquettes

8.1.2. Cylindrical

8.1.3. RUF

8.1.4. Pini Kay

8.1.5. Others

8.2. Europe White Coal Market Size and Forecast, by Application (2025-2032)

8.2.1. Torrefaction

8.2.2. Pyrolysis

8.2.3. Hydrothermal Carbonization

8.2.4. Others

8.3. Europe White Coal Market Size and Forecast, by End Use (2025-2032)

8.3.1. Ceramic

8.3.2. Power Generation

8.3.3. Food & Beverage

8.3.4. Textile Industry

8.3.5. Others

8.4. Europe White Coal Market Size and Forecast, by Country (2025-2032)

8.4.1. UK

8.4.2. France

8.4.3. Germany

8.4.4. Italy

8.4.5. Spain

8.4.6. Sweden

8.4.7. Austria

8.4.8. Rest of Europe

9. Asia Pacific White Coal Market Size and Forecast (by Value Units)

9.1. Asia Pacific White Coal Market Size and Forecast, by Product (2025-2032)

9.1.1. Briquettes

9.1.2. Cylindrical

9.1.3. RUF

9.1.4. Pini Kay

9.1.5. Others

9.2. Asia Pacific White Coal Market Size and Forecast, by Application (2025-2032)

9.2.1. Torrefaction

9.2.2. Pyrolysis

9.2.3. Hydrothermal Carbonization

9.2.4. Others

9.3. Asia Pacific White Coal Market Size and Forecast, by End Use (2025-2032)

9.3.1. Ceramic

9.3.2. Power Generation

9.3.3. Food & Beverage

9.3.4. Textile Industry

9.3.5. Others

9.4. Asia Pacific White Coal Market Size and Forecast, by Country (2025-2032)

9.4.1. China

9.4.2. S Korea

9.4.3. Japan

9.4.4. India

9.4.5. Australia

9.4.6. Indonesia

9.4.7. Malaysia

9.4.8. Vietnam

9.4.9. Taiwan

9.4.10. Bangladesh

9.4.11. Pakistan

9.4.12. Rest of Asia Pacific

10. Middle East and Africa White Coal Market Size and Forecast (by Value Units)

10.1. Middle East and Africa White Coal Market Size and Forecast, by Product (2025-2032)

10.1.1. Briquettes

10.1.2. Cylindrical

10.1.3. RUF

10.1.4. Pini Kay

10.1.5. Others

10.2. Middle East and Africa White Coal Market Size and Forecast, by Application (2025-2032)

10.2.1. Torrefaction

10.2.2. Pyrolysis

10.2.3. Hydrothermal Carbonization

10.2.4. Others

10.3. Middle East and Africa White Coal Market Size and Forecast, by End Use (2025-2032)

10.3.1. Ceramic

10.3.2. Power Generation

10.3.3. Food & Beverage

10.3.4. Textile Industry

10.3.5. Others

10.4. Middle East and Africa White Coal Market Size and Forecast, by Country (2025-2032)

10.4.1. South Africa

10.4.2. GCC

10.4.3. Egypt

10.4.4. Nigeria

10.4.5. Rest of ME&A

11. South America White Coal Market Size and Forecast (by Value Units)

11.1. South America White Coal Market Size and Forecast, by Product (2025-2032)

11.1.1. Briquettes

11.1.2. Cylindrical

11.1.3. RUF

11.1.4. Pini Kay

11.1.5. Others

11.2. South America White Coal Market Size and Forecast, by Application (2025-2032)

11.2.1. Torrefaction

11.2.2. Pyrolysis

11.2.3. Hydrothermal Carbonization

11.2.4. Others

11.3. South America White Coal Market Size and Forecast, by End Use (2025-2032)

11.3.1. Ceramic

11.3.2. Power Generation

11.3.3. Food & Beverage

11.3.4. Textile Industry

11.3.5. Others

11.4. South America White Coal Market Size and Forecast, by Country (2025-2032)

11.4.1. Brazil

11.4.2. Argentina

11.4.3. Rest of South America

12. Company Profile: Key players

12.1. Airex Energy

12.1.1. Company Overview

12.1.2. Financial Overview

12.1.3. Business Portfolio

12.1.4. SWOT Analysis

12.1.5. Business Strategy

12.1.6. Recent Developments

12.2. TorrCoal

12.3. SSGE Bio-Energy Company Ltd.

12.4. ETIA SAS

12.5. Global Bio-Coal Energy Inc.

12.6. Vega Biofuels Inc.

12.7. NextCoal International Inc.

12.8. CSC Bio-Coal Sdn. Bhd.

12.9. Balaji Agro Coal Industries

12.10. Nexgen Energia

12.11. Hind Bio Coal

12.12. KKR Bio Fuels

12.13. BMK Woods

12.14. VIGIDAS PACK

12.15. Ronak Agrotech Engineering

12.16. Green Fuel India

13. Key Findings

14. Industry Recommendations