Agtech Market Global Industry Analysis and Forecast (2026-2032)

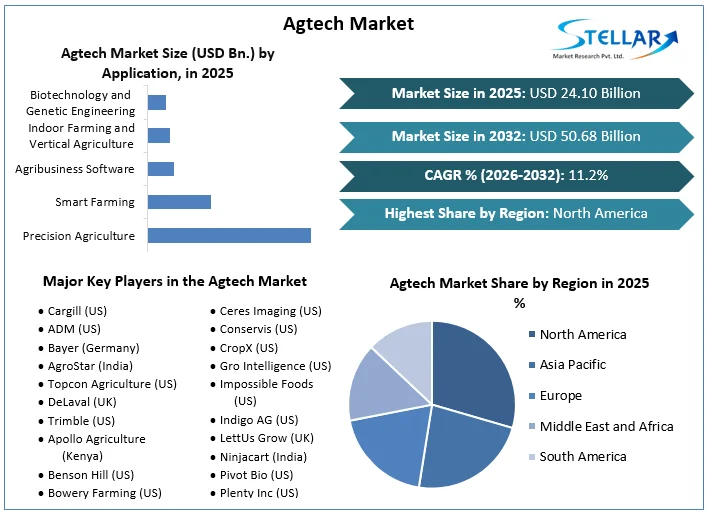

The Agtech Market size was valued at USD 24.10 Bn. in 2025 and the total Global Agtech revenue is expected to grow at a CAGR of 11.2 % from 2026 to 2032, reaching nearly USD 50.68 Bn. by 2032.

Agtech Market Overview

AgTech, also known as agricultural technology, includes the integration of technological innovations into agricultural practices to enhance the efficiency and effectiveness of the production process. The report offers a thorough examination of the agtech market, including key trends, drivers, challenges, and opportunities. It explores the significance of technology in agriculture and provides insights into market segmentation, size, growth patterns, and major players. Agriculture serves as the foundation of the Indian economy, making a substantial contribution to its Gross Domestic Product (GDP) by accounting for 16% and providing employment to 43% of the nation's workforce. Global population projected to reach 10 billion by 2050, the demand for food is intensifying, and necessitating enhanced agricultural productivity.

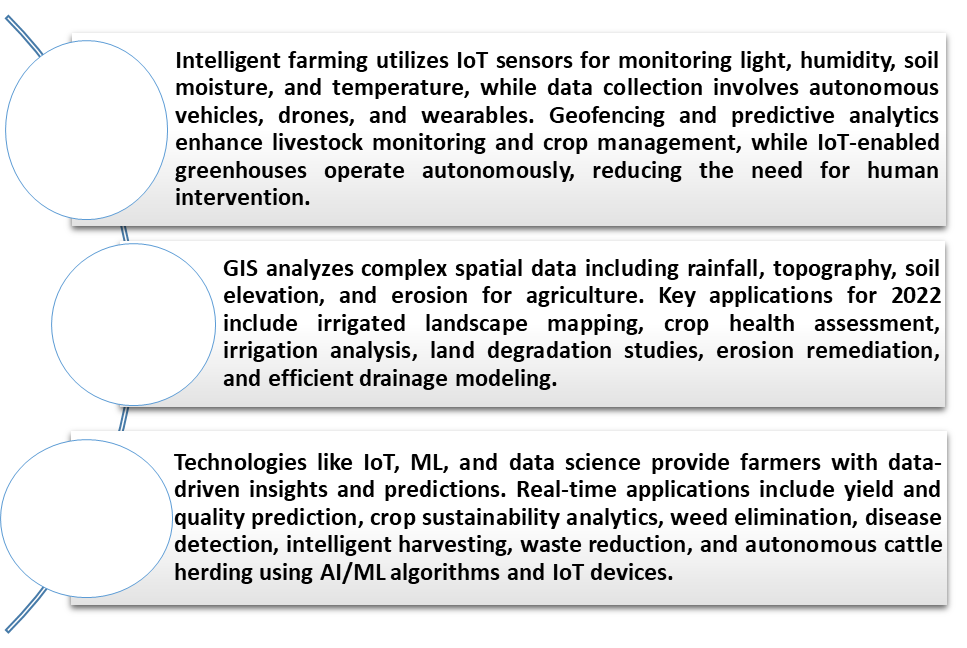

Agtech solutions offer innovative approaches to meet this demand by leveraging IoT, AI, drones, and robotics. These technologies enable precision farming, real-time monitoring, and automation driving efficiency and productivity. Also, climate change-induced challenges such as extreme weather, water scarcity, and soil degradation drive the adoption of Agtech solutions focused on sustainability. Precision irrigation, soil health monitoring, and resilient crop varieties mitigate climate impacts, promoting environmental sustainability in agriculture. The Report provides investment opportunities in precision agriculture, including sensors, drones, GPS-guided machinery, and data analytics, optimizing resource usage, and cutting input costs.

Agribusiness management software enhances farm operations through streamlined inventory tracking, supply chain optimization, and financial analysis. Biotechnology investments target genetic engineering and crop breeding for improved yields, pest resistance, and nutrient optimization. Vertical farming and indoor agriculture, employing hydroponics and controlled environments, cultivate high-value crops in urban areas, reducing transportation and environmental costs. Investments in food traceability technologies address consumer concerns about safety, authenticity, and ethical sourcing, utilizing blockchain and monitoring systems.

To get more Insights: Request Free Sample Report

Agtech Market Dynamics

Integration of Artificial Intelligence (AI) and Machine Learning

AI and machine learning technologies are being integrated into agtech solutions for predictive analytics, crop monitoring, and autonomous machinery, enhancing efficiency and productivity on the farm. Agriculture remains a cornerstone of the Indian economy, sustaining approximately 58% of the population and contributing significantly to the global economy, with an 11.9% share in global agricultural value added, second only to China. Despite a 50% increase in crop production over the past decade, the rate of growth is insufficient to meet the needs of the projected global population of 6 billion by 2030, necessitating accelerated productivity in the agriculture sector.

Globally, investments in smart agricultural systems and technologies, including AI and machine learning (ML), are expected to triple by 2030 to USD 18.2 billion, with AI technologies projected to grow at a compound annual growth rate (CAGR) of 28.5%. Significantly, IoT-enabled agricultural monitoring is expected to be the fastest-growing technology segment, reaching USD 4.5 billion by 2025.

The impact of these technological advancements on the agtech market is significant, with increased investments and expenditures expected in smart agricultural systems and AI technologies. Agtech companies are well-positioned to capitalize on this growth by developing innovative solutions that address the evolving needs of the agriculture sector, driving profitability and sustainability in the industry.

Major digital technologies used in the Agtech Industry:

Data Management and Integration

Agtech solutions often generate vast amounts of data from various sources such as sensors, satellites, drones, and machinery. Managing, integrating, and analyzing the data is effectively challenging for farmers, especially those with limited technical expertise. According to research from SMR, the world is projected to generate over XX zettabytes of data by 2030, underscoring the exponential growth in data volumes. Data originates from a multitude of sources and tools, each employing different formats and terminology to convey information. The diversity is likened to receiving weather updates, soil conditions, and crop details in distinct languages.

Investors stand to gain valuable insights from this data and research, empowering them to make well-informed decisions regarding investment opportunities within the agtech market. Recognizing the growing significance of agricultural data management systems in streamlining farm operations and safeguarding data integrity and compliance, investors pinpoint promising opportunities for investment within the agtech sector. Companies that offer pioneering data management solutions customized for the agricultural domain are poised to capitalize on the surging demand for effective data utilization and protection in contemporary farming practices.

Agtech Market Segment Analysis

By Application, Precision agriculture dominates a substantial and growing portion of the Agtech market, holding 40% of the global market share in 2025. Its impact is profound, optimizing resource allocation such as water and fertilizer to bolster productivity and curtail waste. Through data-driven insights into crop health, soil conditions, and field variability, precision agriculture enhances decision-making processes. It enables the precise application of inputs, minimizing environmental footprint while maximizing efficiency. Examples of precision agriculture technologies include GPS-guided tractors, which ensure precise navigation and operation in the field, enhancing accuracy and reducing overlap.

Variable rate technology enables tailored application of inputs based on real-time data, optimizing resource utilization. Yield monitoring systems provide valuable insights into crop performance, allowing farmers to make informed decisions for future seasons. Also, drone imagery analysis offers detailed and up-to-date information on crop health and field conditions, facilitating proactive management strategies.

- Agritech is experiencing sustained growth globally, with significant disparities in funding across different geographies. As of April 2020, the total global funding for agritech, excluding India, amounted to US$4,083 million, whereas India's total funding reached US$532 million. Among leading geographies, China and North America attracted the highest levels of funding. The disparity in funding reflects varying investment priorities and technological landscapes across regions. Significantly, the "Precision agriculture and farm management" segment emerges as a leader in both funding and the number of startups globally. The segment's prominence underscores the growing focus on leveraging technology to optimize agricultural practices, enhance efficiency, and increase yields.

Agtech Market Regional Insights

North America is poised to lead the global agtech market, driven by several key factors such as the widespread adoption of precision agriculture, with large industrial farms embracing technologies such as drones, GPS systems, and sensor-based irrigation. Additionally, government support through initiatives promoting sustainability and technological integration provides further momentum for market growth. The combination of advanced farming practices and supportive policies positions North America at the lead of the agtech industry, driving innovation and growth in the region. Recent developments in North American agtech highlight a strong focus on precision farming, smart agriculture solutions are experiencing significant growth, including areas such as livestock monitoring, smart greenhouses, and advanced farm management software. Additionally, there is a growing focus on sustainability, particularly in water conservation efforts, which is driving the demand for smart irrigation systems in North America.

Agriculture plays a significant role in North America, cultivating primary crops such as grains, fruits, vegetables, legumes, and plants for non-food purposes. The region manages approximately 3.3 million hectares of organic farmland, a figure that has tripled since 2000, representing around five percent of global organic agricultural land. The region hosts a total of 23,957 organic producers, with approximately 18,000 operating in the United States and over 5,000 in Canada. Presently, the United States leads the organic market with a valuation of 40.6 billion euros. In Canada, per capita consumption of organic products is approximately 84 euros.

The rise in organic agriculture has significant implications for the agtech market in North America. As the demand for organic products continues to rise, there is a corresponding need for advanced agricultural technologies to support organic farming practices. Agtech solutions tailored to organic farming, such as precision organic farming techniques, sustainable soil management systems, and organic pest control methods, are becoming increasingly relevant. Additionally, data-driven analytics and IoT applications help organic farmers optimize resource usage, enhance crop yields, and ensure compliance with organic certification standards. The growing organic agriculture sector in North America presents lucrative opportunities for agtech companies to develop innovative solutions that provide the specific needs and requirements of organic farmers.

Agtech Market Competitive Landscape

In the agtech landscape, established giants such as Cargill, Bayer, and ADM are diversifying by investing in innovative solutions to enhance efficiency. A rise of tech startups is introducing cutting-edge technologies like precision agriculture, AI-driven tools, and indoor farming solutions. These startups inject fresh perspectives into the market. Additionally, robust regional players are making significant strides in sectors like sustainable farming and crop management. Their localized expertise and understanding of regional nuances contribute to the dynamic evolution of the agtech sector, develop the competition, and drive innovation on a global scale.

Emerging technologies such as automated farming machinery, data-driven analytics, and enhanced irrigation systems are revolutionizing agriculture, enabling farmers to optimize resources and increase yields. Agtech innovations also adopt sustainability by reducing water wastage, optimizing fertilizer usage, and enhancing soil health. Also, digital platforms and on-demand services are bridging the gap for small-scale farmers, providing them with greater market access and connecting them with buyers and essential resources. These advancements not only enhance efficiency and productivity but also promote environmentally friendly practices and empower small farmers to participate more effectively in the agricultural marketplace.

- In August 2023, Cargill innovated Nutrition Cloud streamlining livestock feed formulation and reducing costs by $2-to-$5 per ton. The agtech solution empowers farmers to optimize nutrition decisions, maximize animal health, and meet meat quality objectives efficiently, ensuring sustainable and profitable livestock production.

- In Feb 2024, Bayer combines biotechnology, gene editing, and native traits to develop advanced crop varieties tailored to the changing demands of customers, ushering in a new era of agricultural innovation.

|

Agtech Market Scope |

|

|

Market Size in 2025 |

USD 24.10 Bn. |

|

Market Size in 2032 |

USD 50.68 Bn. |

|

CAGR (2026-2032) |

11.2 % |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segment |

By Application Precision Agriculture Smart Farming Agribusiness Software Indoor Farming and Vertical Agriculture Biotechnology and Genetic Engineering |

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Key Player in the Agtech Market

- Cargill (US)

- ADM (US)

- Bayer (Germany)

- AgroStar (India)

- Topcon Agriculture (US)

- DeLaval (UK)

- Trimble (US)

- Apollo Agriculture (Kenya)

- Benson Hill (US)

- Bowery Farming (US)

- Ceres Imaging (US)

- Conservis (US)

- CropX (US)

- Gro Intelligence (US)

- Impossible Foods (US)

- Indigo AG (US)

- LettUs Grow (UK)

- Ninjacart (India)

- Pivot Bio (US)

- Plenty Inc (US)

- AGCO Corporation (US)

- InnovaSea (US)

- Semiosbio (Canada)

- Afimilk (Israel)

- Aker (US)

- XX

Frequently Asked Questions

Agtech contributes to sustainable agriculture by promoting precision farming practices, reducing chemical usage through targeted applications, optimizing water usage with precision irrigation systems, and enhancing soil health through data-driven insights.

Agtech solutions can address climate change challenges in agriculture by providing tools and technologies for climate-smart farming practices, such as precision irrigation, drought-resistant crop varieties, carbon sequestration techniques, and weather monitoring systems, helping farmers adapt to changing environmental conditions and mitigate the impacts of climate change on agricultural productivity.

The Market size was valued at USD 24.10 Billion in 2025 and the total Market revenue is expected to grow at a CAGR of 11.2 % from 2026 to 2032, reaching nearly USD 50.68 billion.

The segments covered in the market report are by Application.

1. Research Methodology

1.1 Research Data

1.1.1. Primary Data

1.1.2. Secondary Data

1.2. Market Size Estimation

1.2.1. Bottom-Up Approach

1.2.2. Top-Down Approach

1.3. Market Breakdown and Data Triangulation

1.4. Research Assumption

2. Agtech Market Executive Summary

2.1. Market Overview

2.2. Market Size (2025) and Forecast (2026– 2032) and Y-O-Y%

2.3. Market Size (USD) and Market Share (%) – By Segments and Regions

3. Global Agtech Market: Competitive Landscape

3.1. SMR Competition Matrix

3.2. Key Players Benchmarking

3.2.1. Company Name

3.2.2. Headquarter

3.2.3. Business Segment

3.2.4. End-user Segment

3.2.5. Y-O-Y%

3.2.6. Revenue (2025)

3.2.7. Profit Margin

3.2.8. Market Share

3.2.9. Company Locations

3.3. Market Structure

3.3.1. Market Leaders

3.3.2. Market Followers

3.3.3. Emerging Players

3.4. Consolidation of the Market

3.4.1. Strategic Initiatives and Developments

3.4.2. Mergers and Acquisitions

3.4.3. Collaborations and Partnerships

3.4.4. New Product/Service Launches and Innovations

4. Agtech Market: Dynamics

4.1. Agtech Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Agtech Market Drivers

4.3. Agtech Market Restraints

4.4. Agtech Market Opportunities

4.5. Agtech Market Challenges

4.6. PORTER’s Five Forces Analysis

4.6.1. Intensity of the Rivalry

4.6.2. Threat of New Entrants

4.6.3. Bargaining Power of Suppliers

4.6.4. Bargaining Power of Buyers

4.6.5. Threat of Substitutes

4.7. PESTLE Analysis

4.7.1. Political Factors

4.7.2. Economic Factors

4.7.3. Social Factors

4.7.4. Technological Factor

4.7.5. Legal Factors

4.7.6. Environmental Factors

4.8. Technological Roadmap

4.9. Regulatory Landscape

4.9.1. Market Regulation by Region

4.9.1.1. North America

4.9.1.2. Europe

4.9.1.3. Asia Pacific

4.9.1.4. Middle East and Africa

4.9.1.5. South America

4.9.2. Impact of Regulations on Market Dynamics

4.9.3. Government Schemes and Initiatives

5. Agtech Market: Global Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

5.1. Agtech Market Size and Forecast, by Application (2025-2032)

5.1.1. Precision Agriculture

5.1.2. Smart Farming

5.1.3. Agribusiness Software

5.1.4. Indoor Farming and Vertical Agriculture

5.1.5. Biotechnology and Genetic Engineering

5.2. Agtech Market Size and Forecast, by Region (2025-2032)

5.2.1. North America

5.2.2. Europe

5.2.3. Asia Pacific

5.2.4. Middle East and Africa

5.2.5. South America

6. North America Agtech Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

6.1. North America Agtech Market Size and Forecast, by Application (2025-2032)

6.1.1. Precision Agriculture

6.1.2. Smart Farming

6.1.3. Agribusiness Software

6.1.4. Indoor Farming and Vertical Agriculture

6.1.5. Biotechnology and Genetic Engineering

6.2. North America Agtech Market Size and Forecast, by Country (2025-2032)

6.2.1. United States

6.2.2. Canada

6.2.3. Mexico

7. Europe Agtech Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

7.1. Europe Agtech Market Size and Forecast, by Application (2025-2032)

7.2. Europe Agtech Market Size and Forecast, by Country (2025-2032)

7.2.1. United Kingdom

7.2.2. France

7.2.3. Germany

7.2.4. Italy

7.2.5. Spain

7.2.6. Sweden

7.2.7. Austria

7.2.8. Rest of Europe

8. Asia Pacific Agtech Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

8.1. Asia Pacific Agtech Market Size and Forecast, by Application (2025-2032)

8.2. Asia Pacific Agtech Market Size and Forecast, by Country (2025-2032)

8.2.1. China

8.2.2. S Korea

8.2.3. Japan

8.2.4. India

8.2.5. Australia

8.2.6. Indonesia

8.2.7. Malaysia

8.2.8. Vietnam

8.2.9. Taiwan

8.2.10. Rest of Asia Pacific

9. Middle East and Africa Agtech Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

9.1. Middle East and Africa Agtech Market Size and Forecast, by Application (2025-2032)

9.2. Middle East and Africa Agtech Market Size and Forecast, by Country (2025-2032)

9.2.1. South Africa

9.2.2. GCC

9.2.3. Nigeria

9.2.4. Rest of ME&A

10. South America Agtech Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

10.1. South America Agtech Market Size and Forecast, by Application (2025-2032)

10.2. South America Agtech Market Size and Forecast, by Country (2025-2032)

10.2.1. Brazil

10.2.2. Argentina

10.2.3. Rest Of South America

11. Company Profile: Key Players

11.1. Cargill (US)

11.1.1. Company Overview

11.1.2. Business Portfolio

11.1.3. Financial Overview

11.1.3.1. Total Revenue

11.1.3.2. Segment Revenue

11.1.3.3. Regional Revenue

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. ADM (US)

11.3. Bayer (Germany)

11.4. AgroStar (India)

11.5. Topcon Agriculture (US)

11.6. DeLaval (UK)

11.7. Trimble (US)

11.8. Apollo Agriculture (Kenya)

11.9. Benson Hill (US)

11.10. Bowery Farming (US)

11.11. Ceres Imaging (US)

11.12. Conservis (US)

11.13. CropX (US)

11.14. Gro Intelligence (US)

11.15. Impossible Foods (US)

11.16. Indigo AG (US)

11.17. LettUs Grow (UK)

11.18. Ninjacart (India)

11.19. Pivot Bio (US)

11.20. Plenty Inc (US)

11.21. AGCO Corporation (US)

11.22. InnovaSea (US)

11.23. Semiosbio (Canada)

11.24. Afimilk (Israel)

11.25. Aker (US)

11.26. XX

12. Key Findings

13. Analyst Recommendations

13.1. Strategic Recommendations

13.2. Future Outlook