Traditional TV and Home Video Market Global Industry Analysis and Forecast (2026-2032)

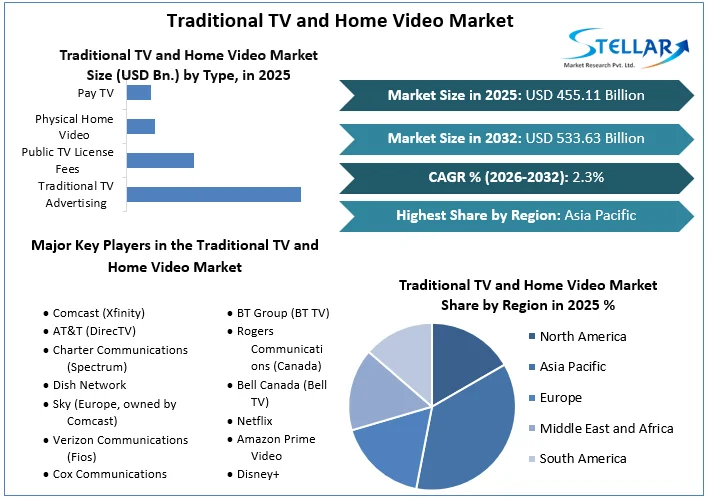

Traditional TV and Home Video Market Size was valued at USD 455.11 Bn. in 2025 and is expected to reach USD 533.63 Bn. by 2032 at a CAGR of 2.3 % over the forecast period.

Traditional TV and Home Video Market Overview

The market for traditional TV and home video has been changing on a global scale. The growing popularity of streaming services like Netflix, Amazon Prime Video, and Disney+ posed problems for traditional TV, which relied on cable and satellite subscriptions. These platforms offered original programming and on-demand material, fueling the global cord-cutting craze. Home video sales concurrently underwent a transition away from tangible formats like DVDs and Blu-rays and toward digital downloads and streaming. Consumers are favouring digital material more and more because of its accessibility and ease. However, the market's environment is extremely dynamic and liable to quick change. Consult recent industry publications and news sources for the most up-to-date information.

To get more Insights: Request Free Sample Report

Traditional TV and Home Video Market Dynamics

The widespread use of smart gadgets and the expansion of high-speed internet access have sped up the transition toward the consumption of digital information. Because viewers can now access a vast library of programming at their convenience, streaming services have grown rapidly, challenging the dominance of conventional cable and satellite TV. The creation of original content by streaming services has been a significant motivator. To draw members and raise the bar for the business, companies like Netflix and Amazon have massively spent in producing unique and appealing episodes and movies. Innovation and competitiveness have been stimulated by this content war. The market has been pushed by shifting customer preferences for individualized and ad-free viewing experiences. Ad-supported TV is in trouble as viewers go to services with no or few ads, which has an effect on ad income for traditional TV networks.

Traditional TV and Home Video Market Restraints

One of the main obstacles is the quick development of streaming services, which has encouraged consumers to cut the cord and resulted in a decline in subscriptions to traditional cable and satellite TV providers. These traditional providers have had to respond to this change and make significant investments in digital offerings, which has raised their costs. Another important barrier is content piracy and illicit streaming, which has been a recurrent problem and costs content producers and distributor’s money. The profitability of the sector is nevertheless threatened by how simple it is to access copyrighted content online without the required license.

Consumers must subscribe to various services in order to get desired material, potentially resulting in subscription fatigue. This fragmented content landscape is the result of competition among streaming platforms. The profitability of streaming platforms is also hampered by high licensing prices. Regulatory obstacles and governmental actions like taxation and content regulation can further confound market dynamics and have an impact on both traditional TV and streaming services. These constraints combined form the shifting worldwide TV and home video market, necessitating innovation and adaptability from market participants.

Traditional TV and Home Video Market Opportunities

To adapt, several traditional TV providers now provide hybrid packages that blend traditional linear TV with streaming and on-demand content. This strategy provides for a wide range of viewing preferences and creates room for expansion. Investing in the creation of original content is still a great opportunity. This approach has been proven effective by streaming platforms, and traditional broadcasters are copying them by developing their own unique programming to draw in and keep viewers. By making their material available worldwide, traditional TV networks and production companies may widen their audience. Digital platforms enable them to access global markets, bringing in new audiences and sources of income. Using targeted advertisements and programmatic advertising together can increase the effectiveness of marketing campaigns.

Traditional broadcasters can make more money by licensing their huge content libraries to streaming platforms and foreign markets. Making use of cutting-edge innovations like 4K/8K broadcasting, augmented reality, and virtual reality can improve the viewing experience and draw in tech-savvy consumers. Partnerships between traditional TV networks and streaming services can foster synergies that are advantageous to both, resulting in the growth of content libraries and distribution systems. Spotting and satisfying specialized content tastes and niche markets can be beneficial. Reaching underrepresented demographics might result in devoted viewers and advertising opportunities.

Traditional TV and Home Video Market Challenge

Fewer people are watching traditional TV as a result of the growth of streaming services. As more consumers take advantage of the adaptability and affordability of streaming services, cable and satellite companies are seeing a rise in cord-cutting and a decline in membership numbers. Piracy is still a problem in the home video industry. Copyrighted content is still being illegally downloaded or streamed, which continues to erode the sources of income for content producers and distributors. Consumers are frustrated by the dispersion of content among different streaming platforms. Multiple subscriptions are frequently required for viewers to obtain the content they want, which raises worries about subscription fatigue.

Traditional TV and Home Video Market Trends

As more people started using streaming services, traditional TV was seeing a loss in viewers and subscriptions. The ease of use, adaptability, and vast content libraries provided by services like Netflix, Amazon Prime Video, and Disney+ were key factors in this transformation. Sales of physical media like DVDs and Blu-rays were continuing to fall in the home video industry. With an increasing focus on 4K Ultra HD and HDR content, digital downloads and streaming services have taken over as the go-to way to watch movies and TV shows The number of new streaming players also increased, escalating the level of competition. By putting money into original content and exclusive license agreements, companies like Apple TV+, HBO Max, and Peacock competed for users.

With a focus on foreign content and localization to appeal to different markets, the global spread of streaming services was remarkable. It's important to understand that the landscape of traditional TV and home video can change quickly owing to changing consumer preferences and technological advancements, so it's best to consult the most recent market reports and news for the newest trends and changes.

Regional Insights for Traditional TV and Home Video Market

Asia-Pacific: The traditional TV and home video market has seen a variety of shifts in the Asia Pacific area. While traditional TV viewing in some nations, such Southeast Asian countries and India, has continued to increase, streaming services have become increasingly popular in many other nations. This transition was spurred by the emergence of in-house streaming platforms and rising internet usage. However, issues like infrastructural discrepancies and content localisation persisted.

North America: The traditional TV and home video market in North America has undergone significant change recently. Even though the established cable and satellite TV providers are still in business, they are up against a lot of competition from streaming services like Netflix, Hulu, and Disney+. Home video sales have also shifted away from traditional DVDs and Blu-ray discs and toward digital forms. The entertainment industry's continuing transition continues to take place largely in North America.

Traditional TV and Home Video Market Segment Analysis

By Type of Service: The type of service provided allows for the segmentation of the global traditional TV and home video market. Broadcast, cable, satellite, and terrestrial alternatives all fall under the category of traditional TV services, which normally air after scheduled programs. These services are well recognized for their linear, appointment-based viewing and mainly rely on advertising revenue. The home video market, in contrast, has made the shift to the digital world and now offers services including physical media, digital downloads, and various kinds of video streaming.

Platforms that provide huge libraries for a monthly fee, such as Netflix, are known as subscription video-on-demand (SVOD) services. Ad-Supported Video-on-Demand (AVOD) and Transactional Video-on-Demand (TVOD) cater to various tastes. The move away from traditional TV, where cord-cutting is still a major trend, is being driven by streaming services, which are investing more and more in original content.

By Type: Traditional TV and Home Video are the two separate market segments that make up the global traditional TV and home video market. Broadcast television in its numerous manifestations, including free-to-air and cable/satellite services, is referred to as traditional TV. With cable, satellite, and terrestrial TV being significant subcategories, it mainly relies on pre-scheduled programming and linear broadcasting. Networks offer ad spots during programs, which is how traditional TV networks largely make money. News and sports are notable categories that are prevalent in this area. However, it has difficulties when viewers switch to more adaptable digital options as a result of cord-cutting trends. There are physical and digital formats available in the home video market. DVDs and Blu-rays are examples of physical media, yet collectors still prize them.

In addition to the emergence of streaming services, digital formats include digital downloads from websites like iTunes and Google Play. The industry has changed as a result of streaming, which can be divided into SVOD (subscription), TVOD (transactional), and AVOD (ad-supported). Streaming companies make significant investments in original content, igniting a global expansion and content conflicts. These market categories demonstrate the dynamic changes in consumer access to and consumption of television and video content across the globe, as the digital sphere is influencing traditional TV more and more.

Traditional TV and Home Video Market: Competitive Landscape

The competitive environment of the worldwide traditional TV and home video market is significantly changing as a result of the continued impact of digital technologies on consumer choices and market dynamics. Streaming services are increasingly challenging conventional broadcast networks and cable companies in the world of traditional TV. Despite the fact that they still have a sizable viewership, the emergence of streaming services like Netflix, Amazon Prime Video, and Disney+ has put their hegemony in jeopardy. These services include convenient anytime /anywhere watching, a big collection of on-demand material, and tailored suggestions. By bundling internet services and their own streaming possibilities, cable and satellite providers are adjusting.

As customers turn more and more to digital downloads and streaming, tangible media like DVDs and Blu-rays are steadily losing market share in the home video sector. Streaming behemoths are battling for subscribers in this competition, which is mostly between digital platforms. The market is becoming even more fragmented as new competitors and regional services emerge in addition to the major ones. The rivalry for premium content rights is also becoming more intense as technological giants like Apple and Amazon make significant investments in the creation of original content. There are bidding wars for exclusive titles since content producers and studios now have more distribution alternatives than ever. Traditional TV and home video providers are being driven to innovate, adapt, and investigate hybrid models as the global market changes in order to stay competitive. A balance is probably what will determine the market's future.

|

Traditional TV and Home Video Market Scope |

|

|

Market Size in 2025 |

USD 455.11 Bn. |

|

Market Size in 2032 |

USD 533.63 Bn. |

|

CAGR (2026-2032) |

2.3 % |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segment Scope |

By Type of Service

|

|

By Type

|

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Traditional TV and Home Video Market Key players

- Comcast (Xfinity)

- AT&T (DirecTV)

- Charter Communications (Spectrum)

- Dish Network

- Sky (Europe, owned by Comcast)

- Verizon Communications (Fios)

- Cox Communications

- BT Group (BT TV)

- Rogers Communications (Canada)

- Bell Canada (Bell TV)

- Netflix

- Amazon Prime Video

- Disney+

Frequently Asked Questions

Asia-Pacific region is expected to dominate the Traditional TV and Home Video Market over the forecast period.

The market size of the Traditional TV and Home Video Market is expected to reach USD 533.63 Billion by 2032.

The major key players in the Global Traditional TV and Home Video Market are Comcast (Xfinity), AT&T (DirecTV), Charter Communications (Spectrum), Dish Network, Sky (Europe, owned by Comcast).

Increasing technological advancements such as implementation of block chain technology and artificial intelligence (AI) to improve the quality of videos are the factors expected to drive the Traditional TV and Home Video Market growth over the forecast period (2026-2032).

1. Research Methodology

1.1 Research Data

1.1.1. Primary Data

1.1.2. Secondary Data

1.2. Market Size Estimation

1.2.1. Bottom-Up Approach

1.2.2. Top-Down Approach

1.3. Market Breakdown and Data Triangulation

1.4. Research Assumption

2. Traditional TV and Home Video Market Executive Summary

2.1. Market Overview

2.2. Market Size (2025) and Forecast (2026 – 2032) and Y-O-Y%

2.3. Market Size (USD) and Market Share (%) – By Segments and Regions

3. Global Traditional TV and Home Video Market: Competitive Landscape

3.1. SMR Competition Matrix

3.2. Key Players Benchmarking

3.2.1. Company Name

3.2.2. Headquarter

3.2.3. Service Segment

3.2.4. End-user Segment

3.2.5. Y-O-Y%

3.2.6. Revenue (2025)

3.2.7. Profit Margin

3.2.8. Market Share

3.2.9. Company Locations

3.3. Market Structure

3.3.1. Market Leaders

3.3.2. Market Followers

3.3.3. Emerging Players

3.4. Consolidation of the Market

3.4.1. Strategic Initiatives and Developments

3.4.2. Mergers and Acquisitions

3.4.3. Collaborations and Partnerships

4. Traditional TV and Home Video Market: Dynamics

4.1. Traditional TV and Home Video Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Traditional TV and Home Video Market Drivers

4.3. Traditional TV and Home Video Market Restraints

4.4. Traditional TV and Home Video Market Opportunities

4.5. Traditional TV and Home Video Market Challenges

4.6. PORTER’s Five Forces Analysis

4.6.1. Intensity of the Rivalry

4.6.2. Threat of New Entrants

4.6.3. Bargaining Power of Suppliers

4.6.4. Bargaining Power of Buyers

4.6.5. Threat of Substitutes

4.7. PESTLE Analysis

4.7.1. Political Factors

4.7.2. Economic Factors

4.7.3. Social Factors

4.7.4. Technological Factor

4.7.5. Legal Factors

4.7.6. Environmental Factors

4.8. Technological Roadmap

4.9. Regulatory Landscape

4.9.1. Market Regulation by Region

4.9.1.1. North America

4.9.1.2. Europe

4.9.1.3. Asia Pacific

4.9.1.4. Middle East and Africa

4.9.1.5. South America

4.9.2. Impact of Regulations on Market Dynamics

4.9.3. Government Schemes and Initiatives

5. Traditional TV and Home Video Market: Global Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

5.1. Traditional TV and Home Video Market Size and Forecast, by Type of Service (2025-2032)

5.1.1. Cable TV

5.1.2. Satellite TV

5.1.3. Terrestrial TV

5.1.4. IPTV

5.1.5. Physical Media

5.1.6. Digital Streaming Services

5.1.7. Live TV streaming Services

5.1.8. Emerging Services

5.2. Traditional TV and Home Video Market Size and Forecast, by Type (2025-2032)

5.2.1. Traditional TV Advertising

5.2.2. Public TV License Fees

5.2.3. Physical Home Video

5.2.4. Pay TV

5.3. Traditional TV and Home Video Market Size and Forecast, by Region (2025-2032)

5.3.1. North America

5.3.2. Europe

5.3.3. Asia Pacific

5.3.4. Middle East and Africa

5.3.5. South America

6. North America Traditional TV and Home Video Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

6.1. North America Traditional TV and Home Video Market Size and Forecast, by Type of Service (2025-2032)

6.1.1. Cable TV

6.1.2. Satellite TV

6.1.3. Terrestrial TV

6.1.4. IPTV

6.1.5. Physical Media

6.1.6. Digital Streaming Services

6.1.7. Live TV streaming Services

6.1.8. Emerging Services

6.2. North America Traditional TV and Home Video Market Size and Forecast, by Type (2025-2032)

6.2.1. Traditional TV Advertising

6.2.2. Public TV License Fees

6.2.3. Physical Home Video

6.2.4. Pay TV

6.3. North America Traditional TV and Home Video Market Size and Forecast, by Country (2025-2032)

6.3.1. United States

6.3.2. Canada

6.3.3. Mexico

7. Europe Traditional TV and Home Video Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

7.1. Europe Traditional TV and Home Video Market Size and Forecast, by Type of Service (2025-2032)

7.2. Europe Traditional TV and Home Video Market Size and Forecast, by Type (2025-2032)

7.3. Europe Traditional TV and Home Video Market Size and Forecast, by Country (2025-2032)

7.3.1. United Kingdom

7.3.2. France

7.3.3. Germany

7.3.4. Italy

7.3.5. Spain

7.3.6. Sweden

7.3.7. Austria

7.3.8. Rest of Europe

8. Asia Pacific Traditional TV and Home Video Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

8.1. Asia Pacific Traditional TV and Home Video Market Size and Forecast, by Type of Service (2025-2032)

8.2. Asia Pacific Traditional TV and Home Video Market Size and Forecast, by Type (2025-2032)

8.3. Asia Pacific Traditional TV and Home Video Market Size and Forecast, by Country (2025-2032)

8.3.1. China

8.3.2. S Korea

8.3.3. Japan

8.3.4. India

8.3.5. Australia

8.3.6. Indonesia

8.3.7. Malaysia

8.3.8. Vietnam

8.3.9. Taiwan

8.3.10. Rest of Asia Pacific

9. Middle East and Africa Traditional TV and Home Video Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

9.1. Middle East and Africa Traditional TV and Home Video Market Size and Forecast, by Type of Service (2025-2032)

9.2. Middle East and Africa Traditional TV and Home Video Market Size and Forecast, by Type (2025-2032)

9.3. Middle East and Africa Traditional TV and Home Video Market Size and Forecast, by Country (2025-2032)

9.3.1. South Africa

9.3.2. GCC

9.3.3. Nigeria

9.3.4. Rest of ME&A

10. South America Traditional TV and Home Video Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

10.1. South America Traditional TV and Home Video Market Size and Forecast, by Type of Service (2025-2032)

10.2. South America Traditional TV and Home Video Market Size and Forecast, by Type (2025-2032)

10.3. South America Traditional TV and Home Video Market Size and Forecast, by Country (2025-2032)

10.3.1. Brazil

10.3.2. Argentina

10.3.3. Rest Of South America

11. Company Profile: Key Players

11.1. Comcast (Xfinity)

11.1.1. Company Overview

11.1.2. Business Portfolio

11.1.3. Financial Overview

11.1.3.1. Total Revenue

11.1.3.2. Segment Revenue

11.1.3.3. Regional Revenue

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. AT&T (DirecTV)

11.3. Charter Communications (Spectrum)

11.4. Dish Network

11.5. Sky (Europe, owned by Comcast)

11.6. Verizon Communications (Fios)

11.7. Cox Communications

11.8. BT Group (BT TV)

11.9. Rogers Communications (Canada)

11.10. Bell Canada (Bell TV)

11.11. Netflix

11.12. Amazon Prime Video

11.13. Disney+

12. Key Findings

13. Analyst Recommendations

13.1. Strategic Recommendations

13.2. Future Outlook