Open-Angle Glaucoma Market - Global Industry Analysis and Forecast (2025-2032)

The Open-Angle Glaucoma Market size was valued at USD 5.67 Billion in 2024 and the total Open-Angle Glaucoma Market size is expected to grow at a CAGR of 6.5% from 2025 to 2032, reaching nearly USD 9.39 Billion by 2032.

Open-Angle Glaucoma Market Overview

Open-Angle Glaucoma is a chronic eye disease, that causes progressive loss of vision by damaging the optic nerve. Although there is no known treatment for glaucoma, there are many ways to manage the condition and stop it from getting worse. These treatments aim to lower intraocular pressure (IOP), which is a major contributing factor to glaucoma-related optic nerve damage. Glaucoma treatment is growing significantly, per the Stellar analysis research. Increasing glaucoma prevalence, advancements in treatment options, increased public awareness and screening initiatives, growing healthcare costs, and regional differences are some of the factors contributing to this trend. When treatment for open-angle glaucoma, monotherapy is still the recommended course of action.

Combination medications are often reserved for situations in which monotherapy has not produced a low enough IOP. Applying topically given monotherapy has several limitations. Combination medications address the issues where monotherapy is unable to reduce IOP in certain circumstances and eventually becomes less effective. Combination medication products try to target many targets or pathways of action to treat the disease with the least amount of side effects possible. Compared to using both components alone, FDCs are preferable in combination therapy to support patient adherence and persistence for treatment. FDCs provide vital alternatives for patients who need more than one medicine to regulate IOP in the treatment of open-angle glaucoma, making them significant adjuncts to the variety of open-angle glaucoma medications now available.

- Glaucoma is the third most common cause of blindness in the general population and is one of the most common eye disorders seen in primary and secondary care systems. Over time, glaucoma worsens and causes damage to the optic nerve of the eye. It usually has to do with elevated intraocular pressure. An increase in intraocular pressure in your eye harms the optic nerve, which sends images to your brain.

To get more Insights: Request Free Sample Report

Open-Angle Glaucoma Market Dynamics

Trends in the Open-Angle Glaucoma Market

A major advance in the open-angle glaucoma treatment industry is the growing public awareness of glaucoma. One of the main causes of vision loss and blindness in the world today is glaucoma. Glaucoma is frequently asymptomatic and invisible in its early stages. Glaucoma is treatable and frequently be prevented from causing serious vision loss if detected early before major vision loss develops.

Medical ophthalmologists, surgeons, and pathologists must collaborate in a coordinated, integrative effort to diagnose eye problems, including glaucoma, in addition to raising public awareness of the condition. Awareness campaigns and sophisticated diagnostic methods in the field of ophthalmology aid in the detailed diagnosis of glaucoma, allowing ophthalmology to recommend the best course of action for patients. This has a favorable effect on the growth of the open-angle glaucoma therapeutics market globally over the projected period.

Drivers in the Open-Angle Glaucoma Market

The market treatments for open-angle glaucoma are growing thanks to a solid path and recent approvals. Pharmaceutical companies have been making significant investments in the development of new medications to treat open-angle glaucoma due to its high occurrence. Additionally, several businesses recently got permission for their medications to treat open-angle glaucoma. Additionally, there is 0.002% omidenepag isopropyl in the ophthalmic solution. This drug has been demonstrated to lower IOP, thus people with open-angle glaucoma or ocular hypertension find benefit from it. Thus, throughout the projected period, the development of the global open-angle glaucoma therapies market is expected to be driven by recently approved pharmaceuticals and late-stage clinical drugs. With less reliance on medication and longer-lasting comfort, non-pharmacological glaucoma treatment valor leads to growth in the market. Other treatment options for glaucoma include laser therapy, selective laser trabeculoplasty, and minimally invasive glaucoma procedures (MIGs). With either technique, the patient's eye produces more fluid, which lowers intraocular pressure.

- The market is expected to increase more rapidly with oral medications. The sector is expected to grow the global market since the majority of the medications are offered in tablet and capsule form, which is a very practical mode of administration, particularly for the senior population.

Restraints in Open-Angle Glaucoma Market

The glaucoma treatment approval process is stringent, and sometimes a product has to be withdrawn or rejected from the market due to safety concerns or for a variety of other reasons, such as toxicity, PH properties, bioavailability, pharmacological performance, and effectiveness. For instance, in 2023, Apotex Corp. canceled 22,027 bottles of timolol maleate ophthalmic solution because of the failure of medicine samples to meet stability requirements. Drug side effects are occasionally linked to glaucoma therapy. For example, beta-blockers induce low blood pressure and decreased drive prostaglandin analogs cause itching and redness in the eyes, and Rho kinase inhibitors produce stinging and little hemorrhage on the white part of the eye. Significant drug recalls for the treatment have a big impact on market growth. For instance, before their delivery to patients, Allergan was compelled to remove one lot of Lumigan and seven lots of Combigan due to their failure to meet regulatory requirements and impurity levels. Medication advertised for the treatment of glaucoma causes patients and healthcare professionals to become suspicious and concerned in the wake of regulatory recalls of such goods. Technology that promises efficacy, long-term benefits, and low side effects also has an impact on treatment acceptability in this industry. Consequently, it is expected to restrict market share.

Opportunities in Open-Angle Glaucoma Market

Growing sales of novel products and clinical trial supplies support the industry's expansion. A groundbreaking medication for the treatment of glaucoma is developed in 2024 thanks to collaboration between the Institute for Therapeutics Discovery & Development (ITDD) and the Department of Medicinal Chemistry at the University of Minnesota College of Pharmacy. Driving the market are the ophthalmology sector's rapid technical advancements and the growing adoption of novel surgical techniques. Technology advancements in optical coherence tomography (OCT), medical imaging, micro-invasive glaucoma surgery (MIGS), selective laser trabeculoplasty (SLT), and progression analysis software have raised the need for optometrists. This constitutes a major catalyst for market growth. The glaucoma market is expected to increase in size as prescription drugs and laser therapy become more widely available.

- Opportunities for market growth are created by the rise in the number of retail pharmacies in highly developed nations and the increase in the number of open-angle glaucoma medications supplied through these establishments. Additionally, because retail pharmacies sell drugs more conveniently, patients prefer to buy them there.

Open-Angle Glaucoma Market Segment Analysis

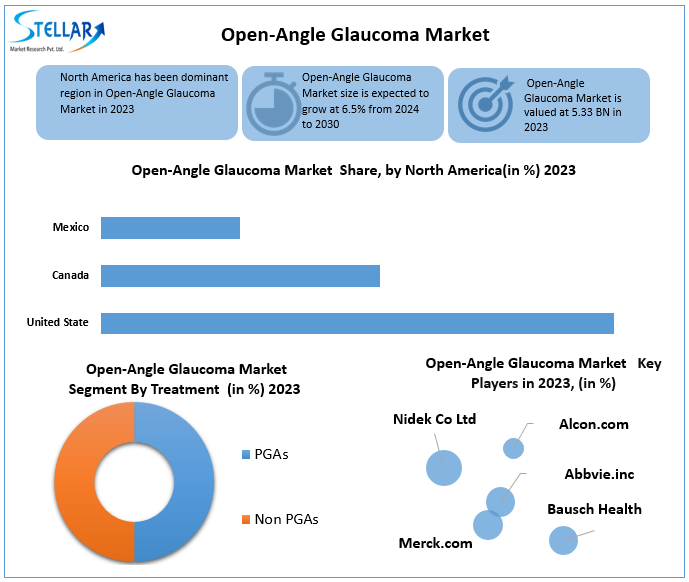

Based on, Treatment, PGAs Open-angle glaucoma is treated with PGAs as the initial course of action. There are three PGAs on the market right now bimatoprost (0.03%), latanoprost (0.005%), and travoprost (0.004%). Comparing the aforesaid medications in combination with monotherapy, however, reveals a high level of efficacy. Changes in extracellular matrix components and ciliary muscle relaxation are the exact mechanisms by which prostaglandins increase uveoscleral outflow. Stinging and burning, changes in eye color, and lashes that lengthen and curl are all potential side effects of PGAs. Given the growing prevalence of PGA combinations, the global market in open-angle glaucoma therapies is expected to increase at a rapid rate throughout the forecast period due to the PGA sector.

Non-PGAs, In addition to PGAs, there are other medications on the market called non-PGAs that are used to treat open-angle glaucoma. These medications inhibit the generation of aqueous humor. The non-PGA sector includes multiple medication classes. Beta-blockers work by reducing the generation of aqueous humor, which lowers IOP. Hydrochloric acid secretion in the ciliary epithelium is reduced when cyclic adenosine monophosphate production is inhibited. Adrenergic agonists lower intraocular pressure (IOP) via increasing aqueous outflow through a secondary mechanism and mediating aqueous suppression. There are multiple ways in which nonselective adrenergic agonists, including epinephrine, lower intraocular pressure. The availability of numerous medications and affordable generics is the main factor driving this segment's rise. However, it's estimated that the negative impacts of non-PGAs resolve impede their growth.

Based on, Disease Type, Open-Angle glaucoma is the most common type, accounting for the majority of incidents. It is characterized by a gradual, usually painless increase in intraocular pressure (IOP) brought on by an obstruction in the trabecular meshwork, the drainage system of the eye. The term "primary open-angle glaucoma" (POAG) is used when the cause of OAG is unrelated to other eye conditions.

Angle-closure glaucoma is more severe and symptomatic than open-angle glaucoma, but it is less common. The abrupt surge in intraocular pressure (IOP) is caused by obstruction of the drainage angle between the iris and cornea. Both primary and secondary ACGs (associated with other eye conditions) occur when there is no underlying eye disease causing the closure.

Based On Distribution Channel, Hospital Pharmacy Pharmaceutical companies and hospitals have partnered to demonstrate the importance of the hospital pharmacy distribution channel in the open-angle glaucoma treatments market. The rising initiatives aimed at improving access to healthcare drive the rising prevalence of open-angle glaucoma, the aging population, the growth of healthcare infrastructure, and the rising demand for glaucoma medicines in hospitals. This, in turn, boosts the growth of the global market in hospital pharmacy-based therapies for open-angle glaucoma during the forecast period.

Open-Angle Glaucoma Market Regional Analysis

North America during the forecast period, North America is expected to contribute 51% of the growth of the global market. The geographical trends and drivers that influence the market throughout the forecast period have been thoroughly discussed by Stellar Analysis. The increasing prevalence of glaucoma in North America is the main reason for the market growth. Three million Americans suffer from glaucoma, according to the Centers for Disease Control and Prevention (CDC). It ranks as the second most prevalent cause of blindness globally. Open-angle glaucoma, which causes an increase in ocular pressure, is the most prevalent type of glaucoma. Because it frequently lacks early signs, 50% of glaucoma sufferers are unaware that they have the condition. Because eye problems are very common in this area, public groups and merchants have also raised awareness of these diseases through various teaching programs. The usage of open-angle glaucoma therapies is expected to rise in the region due to growing awareness of eye illnesses. This is propelling the growth of the regional market throughout the forecast period.

- North America's main countries covered by the open-angle glaucoma market research are the United States, Canada, and Mexico. Also, the annual cost of direct glaucoma expenses to the US economy is estimated to be $2.86 billion, not including lost productivity. Additionally, glaucoma awareness is being raised by several American organizations, which is expected to fuel the market's overall expansion.

Asia Pacific grows at the fastest rate new drug introductions are among the recent advancements in the treatment options for many diseases. Patients with severe or refractory glaucoma in particular should be able to choose safer and more effective options thanks to these advancements. The market is affected by the following factors insurance plans, government regulations, the quality of the healthcare system, and the frequency of the disease.

Open-Angle Glaucoma Market Competitive Landscape

The market adoption lifecycle, which covers from the innovator's stage to the laggard's stage, is included in the market competitive landscape analysis. It focuses on adoption rates according to penetration in various geographical areas. To assist businesses in assessing and formulating their growth strategy, the report also provides important purchasing criteria and price sensitivity drivers.

- On January 16th, 2024, six specialist fundus cameras that capture images of the retina, or back of the eye were donated to help Orbis increase its AI-powered diabetic retinopathy screening program in Vietnam.

- Alcons The significance of Vivity's unique, patented wavefront-shaping technology, which makes presbyopia correction easier for patients and surgeons, is highlighted by Milestone on March 27, 2024.

|

Open-Angle Glaucoma Market Scope |

|

|

Market Size in 2024 |

USD 5.67 Bn. |

|

Market Size in 2032 |

USD 9.39 Bn. |

|

CAGR (2025-2032) |

6.5% |

|

Historic Data |

2019-2024 |

|

Base Year |

2024 |

|

Forecast Period |

2024-2030 |

|

Segment Scope |

By Treatment

|

|

By Disease Type

|

|

|

By Distribution Channel

|

|

|

By Drug Class

|

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Austria, and Rest of Europe Asia Pacific – China, India, Japan, Soth Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Key Player in the Open-Angle Glaucoma Market

- Nidek Co Ltd

- Alcon.com

- Abbvie, Inc

- Bausch Health

- Merck.com

- Pfizer Inc

- Fera Pharmaceuticals

- EyePoint Pharmaceuticals,Inc

- Amorphex Therapeutics

- Kubota Vision Inc

- Astellas Pharma Inc

- Scope Eye Care

- Santen Pharmaceutical Co. Ltd.

- Novartis

- Thea UK

- Alembic Pharmaceuticals Ltd.

- IRIDEX

- Bayer AG

- Zeiss.com

- Bausch + Lomb Corporation

Frequently Asked Questions

An analysis of profit trends and projections for companies in the Open-Angle Glaucoma Market is included, offering insights into factors driving profitability, cost management strategies, and financial performance metrics.

The forecast period of the market is 2025 to 2032.

The Open-Angle Glaucoma Market size was valued at USD 5.67 Billion in 2024 and the total Open-Angle Glaucoma Market size is expected to grow at a CAGR of 6.5% from 2025 to 2032, reaching nearly USD 9.39 Billion by 2032.

The segments covered in the market report are By Treatment Type, By Disease Type, By Distribution Channel, and By Drug class.

1. Open-Angle Glaucoma Market: Research Methodology

2. Open-Angle Glaucoma Market: Executive Summary

3. Open-Angle Glaucoma Market: Competitive Landscape

4. Potential Areas for Investment

4.1. Stellar Competition Matrix

4.2. Competitive Landscape

4.3. Key Players Benchmarking

4.4. Market Structure

4.4.1. Market Leaders

4.4.2. Market Followers

4.4.3. Emerging Players

4.5. Consolidation of the Market

5. Open-Angle Glaucoma Market: Dynamics

5.1. Market Driver

5.1.1. Increasing Consumer Awareness

5.1.2. Innovation in Product Offerings

5.2. Market Trends by Region

5.2.1. North America

5.2.2. Europe

5.2.3. Asia Pacific

5.2.4. Middle East and Africa

5.2.5. South America

5.3. Market Drivers by Region

5.3.1. North America

5.3.2. Europe

5.3.3. Asia Pacific

5.3.4. Middle East and Africa

5.3.5. South America

5.4. Market Restraints

5.5. Market Opportunities

5.6. Market Challenges

5.7. PORTER’s Five Forces Analysis

5.8. PESTLE Analysis

5.9. Strategies for New Entrants to Penetrate the Market

5.10. Regulatory Landscape by Region

5.10.1. North America

5.10.2. Europe

5.10.3. Asia Pacific

5.10.4. Middle East and Africa

5.10.5. South America

6. Open-Angle Glaucoma Market Size and Forecast by Segments (by value Units)

6.1. Open-Angle Glaucoma Market Size and Forecast, by Treatment (2024-2032)

6.1.1. PGAs

6.1.2. Non-PGAs

6.2. Open-Angle Glaucoma Market Size and Forecast, by Disease Type (2024-2032)

6.2.1. Open Angle Glaucoma

6.2.2. Angle Closure Glaucoma

6.2.3. Other

6.3. Open-Angle Glaucoma Market Size and Forecast, by Distribution Channel (2024-2032)

6.3.1. Hospital Pharmacies

6.3.2. Retail Pharmacies

6.3.3. Online Pharmacies

6.4. Open-Angle Glaucoma Market Size and Forecast, by Drug Class (2024-2032)

6.4.1. Prostaglandin Analog

6.4.2. Beta Blockers

6.4.3. Adrenergic Agonist

6.4.4. Carbonic Anhydrase Inhibitors

6.4.5. Others

6.5. Open-Angle Glaucoma Market Size and Forecast, by Region (2024-2032)

6.5.1. North America

6.5.2. Europe

6.5.3. Asia Pacific

6.5.4. Middle East and Africa

6.5.5. South America

7. North America Open-Angle Glaucoma Market Size and Forecast (by value Units)

7.1. North America Open-Angle Glaucoma Market Size and Forecast, by Treatment (2024-2032)

7.1.1. PGAs

7.1.2. Non-PGAs

7.2. North America Open-Angle Glaucoma Market Size and Forecast, by Disease Type (2024-2032)

7.2.1. Open Angle Glaucoma

7.2.2. Angle Closure Glaucoma

7.2.3. Other

7.3. North America Open-Angle Glaucoma Market Size and Forecast, by Distribution Channel (2024-2032)

7.3.1. Hospital Pharmacies

7.3.2. Retail Pharmacies

7.3.3. Online Pharmacies

7.4. North America Open-Angle Glaucoma Market Size and Forecast, by Drug class (2024-2032)

7.4.1. Prostaglandin Analog

7.4.2. Beta Blockers

7.4.3. Adrenergic Agonist

7.4.4. Carbonic Anhydrase Inhibitors

7.4.5. Others

7.5. North America Open-Angle Glaucoma Market Size and Forecast, by Country (2024-2032)

7.5.1. United States

7.5.2. Canada

7.5.3. Mexico

8. Europe Open-Angle Glaucoma Market Size and Forecast (by Value Units)

8.1. Europe Open-Angle Glaucoma Market Size and Forecast, by Treatment (2024-2032)

8.1.1. PGAs

8.1.2. Non-PGAs

8.2. Europe Open-Angle Glaucoma Market Size and Forecast, by Disease Type (2024-2032)

8.2.1. Open Angle Glaucoma

8.2.2. Angle Closure Glaucoma

8.2.3. Other

8.3. Europe Open-Angle Glaucoma Market Size and Forecast, by Distribution Channel (2024-2032)

8.3.1. Hospital Pharmacies

8.3.2. Retail Pharmacies

8.3.3. Online Pharmacies

8.4. Europe Open-Angle Glaucoma Market Size and Forecast, by Drug class (2024-2032)

8.4.1. Prostaglandin Analog

8.4.2. Beta Blockers

8.4.3. Adrenergic Agonist

8.4.4. Carbonic Anhydrase Inhibitors

8.4.5. Others

8.5. Europe Open-Angle Glaucoma Market Size and Forecast, by Country (2024-2032)

8.5.1. UK

8.5.2. France

8.5.3. Germany

8.5.4. Italy

8.5.5. Spain

8.5.6. Sweden

8.5.7. AustriaValue

8.5.8. Rest of Europe

9. Asia Pacific Open-Angle Glaucoma Market Size and Forecast (by Value Units)

9.1. Asia Pacific Open-Angle Glaucoma Market Size and Forecast, by Treatment (2024-2032)

9.1.1. PGAs

9.1.2. Non-PGAs

9.2. Asia Pacific Open-Angle Glaucoma Market Size and Forecast, by Disease Type (2024-2032)

9.2.1. Open Angle Glaucoma

9.2.2. Angle Closure Glaucoma

9.2.3. Other

9.3. Asia Pacific Open-Angle Glaucoma Market Size and Forecast, by Distribution Channel (2024-2032)

9.3.1. Hospital Pharmacies

9.3.2. Retail Pharmacies

9.3.3. Online Pharmacies

9.4. Asia Pacific Open-Angle Glaucoma Market Size and Forecast, by Drug class (2024-2032)

9.4.1. Prostaglandin Analog

9.4.2. Beta Blockers

9.4.3. Adrenergic Agonist

9.4.4. Carbonic Anhydrase Inhibitors

9.4.5. Others

9.5. Asia Pacific Open-Angle Glaucoma Market Size and Forecast, by Country (2024-2032)

9.5.1. China

9.5.2. S Korea

9.5.3. Japan

9.5.4. India

9.5.5. Australia

9.5.6. Asean

9.5.7. Rest of Asia Pacific

10. Middle East and Africa Open-Angle Glaucoma Market Size and Forecast (by Value Units)

10.1. Middle East and Africa Open-Angle Glaucoma Market Size and Forecast, by Treatment (2024-2032)

10.1.1. PGAs

10.1.2. Non-PGAs

10.2. Middle East and Africa Open-Angle Glaucoma Market Size and Forecast, by Disease Type (2024-2032)

10.2.1. Open Angle Glaucoma

10.2.2. Angle Closure Glaucoma

10.2.3. Other

10.3. Middle East and Africa Open-Angle Glaucoma Market Size and Forecast, by Distribution Channel (2024-2032)

10.3.1. Hospital Pharmacies

10.3.2. Retail Pharmacies

10.3.3. Online Pharmacies

10.4. Middle East and Africa Open-Angle Glaucoma Market Size and Forecast, by Drug class (2024-2032)

10.4.1. Prostaglandin Analog

10.4.2. Beta Blockers

10.4.3. Adrenergic Agonist

10.4.4. Carbonic Anhydrase Inhibitors

10.4.5. Others

10.5. Middle East and Africa Open-Angle Glaucoma Market Size and Forecast, by Country (2024-2032)

10.5.1. South Africa

10.5.2. GCC

10.5.3. Rest of ME&A

11. South America Open-Angle Glaucoma Market Size and Forecast (by Value Units)

11.1. South America Open-Angle Glaucoma Market Size and Forecast, by Treatment (2024-2032)

11.1.1. PGAs

11.1.2. Non-PGAs

11.2. South America Open-Angle Glaucoma Market Size and Forecast, by Disease Type (2024-2032)

11.2.1. Open Angle Glaucoma

11.2.2. Angle Closure Glaucoma

11.2.3. Other

11.3. South America Open-Angle Glaucoma Market Size and Forecast, by Distribution Channel (2024-2032)

11.3.1. Hospital Pharmacies

11.3.2. Retail Pharmacies

11.3.3. Online Pharmacies

11.4. South America Open-Angle Glaucoma Market Size and Forecast, by Drug class (2024-2032)

11.4.1. Prostaglandin Analog

11.4.2. Beta Blockers

11.4.3. Adrenergic Agonist

11.4.4. Carbonic Anhydrase Inhibitors

11.4.5. Others

11.5. South America Open-Angle Glaucoma Market Size and Forecast, by Country (2024-2032)

11.5.1. Brazil

11.5.2. Argentina

11.5.3. Rest of South America

12. Company Profile: Key players

12.1. Nidek Co Ltd

12.1.1. Company Overview

12.1.2. Financial Overview

12.1.3. Business Portfolio

12.1.4. SWOT Analysis

12.1.5. Business Strategy

12.1.6. Recent Developments

12.2. Alcon.com

12.3. Abbvie, Inc

12.4. Bausch Health

12.5. Merck.com

12.6. Pfizer Inc

12.7. Fera Pharmaceuticals

12.8. EyePoint Pharmaceuticals,Inc

12.9. Amorphex Therapeutics

12.10. Kubota Vision Inc

12.11. Astellas Pharma Inc

12.12. Scope Eye Care

12.13. Santen Pharmaceutical Co. Ltd.

12.14. Novartis

12.15. Thea UK

12.16. Alembic Pharmaceuticals Ltd.

12.17. IRIDEX

12.18. Bayer AG

12.19. Zeiss.com

12.20. Bausch + Lomb Corporation

13. Key Findings

14. Industry Recommendation