Europe Coffee Market: Industry Analysis and Forecast (2024-2030)

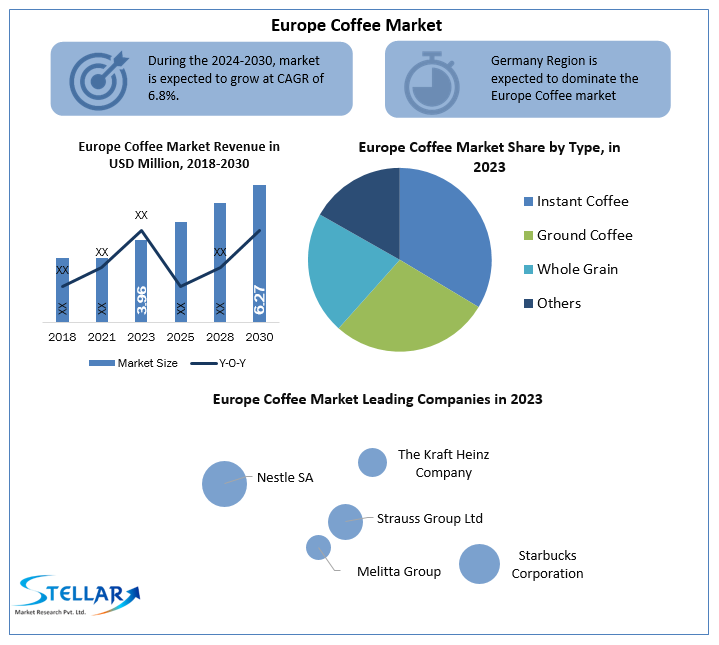

Europe Coffee Market size is volume at 3.96 Mn. tonnes in 2023. Coffee will encourage a great deal of transformation in Beverage Sector in Europe.

Format : PDF | Report ID : SMR_89

Europe Coffee Market Definition:

Coffee is one of the most consumed brewed drinks. Roasted coffee beans are frequently used to make it. These beans are the seeds of berries produced by certain coffee species. Coffee beans are collected, processed, and then dried when their color changes from green to vivid red. The ripeness of the berries is indicated by a change in color. Due to the presence of caffeine in the beverage, coffee has a revitalizing effect. The Universal Trade Zone (UTZ) accreditation program is the largest in the coffee and cocoa industries. Certified coffee provides consumers with assurances regarding the product's dependability. The certificate's goal is to make sustainable farming the norm by encouraging farmers to use environmentally friendly agricultural practices. Certifications such as Fair-Trade Certification, Rainforest Alliance Certification, and UTZ Certification are followed by industry players.

To get more Insights: Request Free Sample Report

Europe Coffee Market Dynamics:

Europe is the largest and most important market for coffee. This is reflected in the ever-growing number of European specialty roasters, coffee shops, and local coffee brands, as well as the more knowledgeable and discerning European coffee consumers.

Coffee shops and small and medium-sized coffee roasters are pioneers in introducing high-quality coffee. The European coffee market is driven by several factors, including increasing demand for certified coffee products, consumer acceptance of single-serve coffee brewing systems, and constant innovation led by the top players in the coffee market. Changing weather conditions play a decisive role in coffee production in producing countries and thus affect the supply chain of coffee imported into European countries.

The Premiumization of whole bean coffee products is driving the coffee market. Large companies in the market introduce premium products by using craftsmanship or by using the handpick method to obtain premium products. These factors are expected to drive the demand for coffee in the market.

With the rise of today's younger generation of cafe culture and rising disposable income, employee demography, urbanization, and hospitality are several factors driving the growth of the market in Europe region. Germany and Spain are the largest consumers of organic and traditional coffee in Europe. Germany is also a major importer of organic coffee in Europe.

Changes in labor culture, especially in the corporate industry as well as improving living standards are driving the demand for coffee. Companies and emerging modern brands that are revising their service strategies to increase customer satisfaction and thus loyalty are other factors that are surging the coffee market in Europe. Increasing demand for organic varieties due to increased awareness of the health benefits of coffee. With the introduction of various flavors such as baristas, CCDs, and Starbucks, the customer experience scenario has been enhanced.

The continuous growth of out-of-home consumption is driving the growth of the coffee market in the region. The coffee shops in European countries are leading the way by introducing sophisticated, high-value varieties to consumers which are boosting the demand for the product in the market.

Growing consumer interest in how the coffee is brewed, as well as how the crop is grown. It has become essential for specialty coffee producers to tell the story behind their coffee, its origin, and its other environmental and social aspects. This factor is driving the demand for coffee and attracting new consumers in this region.

Artisan Coffee focuses on quality and care throughout the supply chain. Beverage specialties can stand out from the competition through a variety of roasting, brewing, or manufacturing methods. Combinations with small roasters and local roasters. Players by procuring a variety of ingredients locally and creating a coffee culture in their community are one of the major strategies.

Europe Coffee Market Development:

In 2020, Nestlé Nespresso SA announced an investment of CHF 160 million to expand its production center in Romont, Switzerland, to meet growing consumer demand for premium coffees and international development assistance through the forecast period.

In 2020, Maxwell House launched the new Zero Waste Single Serve coffee pods. It is made entirely from plant materials. All components of the case and its inner bag are 100% compostable, and the outer box is 100% recyclable, leaving no waste for the consumer.

In 2019, Nestlé launched a new coffee product line under the Starbucks brand. The new product line includes 24 products, including whole beans, roasted and ground, as well as Starbucks capsules developed using proprietary Nespresso and Nescafe Dolce Gusto coffee and system technology.

Europe Coffee Market Segment Analysis:

By Source, the Arabica segment is growing popular in the European region. Arabica beans are fairly flat and elongated. Arabica coffee beans have a smoother, more aromatic, and more flavourful taste compared to Robusta. Arabica beans have a caffeine content of approximately 1.5%. These factors are driving the demand of the segment in the market.

Robusta is one of the major preferences for coffee consumers because of its high caffeine content, which makes them less sour and much stronger. Robusta is less susceptible to pests and diseases than Arabica. Its beans are smaller and rounder than Arabica beans. When roasted, Robusta beans generally have a stronger and harsher taste than Arabica, which is often described as bitter.

By Type, in the Europe region, instant Coffee is gaining more popularity. People are using various forms of instant coffee as environmentally responsible coffee pod replacements. Before Lockdown, these consumers crowd grabbed coffee at a drive-through or used their break room’s Keurig. They seek speed, savings, and convenience, but they don’t want to sacrifice flavor..

By Process, the caffeinated segment is majorly popular in this region. Caffeine is the most widely consumed psychotropic drug across the globe and some of its behavioral effects are similar to cocaine, amphetamines, and other stimulants. Arabica beans and Robusta beans are widely used because they contain caffeine.

The objective of the report is to present a comprehensive analysis of the Europe Coffee market to the stakeholders in the industry. The report provides trends that are most dominant in the Europe Coffee market and how these trends will influence new business investments and market development throughout forecast period. The report also aids in the comprehension of the Europe Coffee Market dynamics and competitive structure of market by analyzing market leaders, market followers and regional players.

The qualitative and quantitative data provided in the Europe Coffee market report is to help understand which market segments, regions are expected to grow at higher rates, factors affecting the market, and key opportunity areas, which will drive the industry and market growth through the forecast period. The report also includes the competitive landscape of key players in the industry along with their recent developments in the Europe Coffee market. The report studies factors such as company size, market share, market growth, revenue, production volume, and profits of the key players in the Europe Coffee market.

The report provides Porter's Five Force Model, which helps in designing the business strategies in the market. The report helps in identifying how many rivals are existing, who they are and how their product quality is in Europe Coffee market. The report also analyses if the Europe Coffee market is easy for a new player to gain a foothold in the market, do they enter or exit the market regularly if the market is dominated by a few players, etc.

The report also includes a PESTEL Analysis, which aids in the development of company strategies. Political variables help in figuring out how much a government can influence the Europe Coffee market. Economic variables aid in the analysis of economic performance drivers that have an impact on the Europe Coffee market. Understanding the impact of the surrounding environment and the influence of ecological concerns on the Europe Coffee market is aided by legal factors.

Europe Coffee Market Scope:

|

Europe Coffee Market |

|

|

Market Size in 2023 |

USD 3.96 Mn |

|

Market Size in 2030 |

USD 6.27 Mn |

|

CAGR (2024-2030) |

6.8% |

|

Historic Data |

2018-2022 |

|

Base Year |

2023 |

|

Forecast Period |

2024-2030 |

|

Segment Scope |

By Source

|

|

By Type

|

|

|

By Process

|

|

|

Country Scope |

|

KEY PLAYERS:

- Nestle SA

- The Kraft Heinz Company

- Strauss Group Ltd

- Melitta Group

- Starbucks Corporation

- Luigi Lavazza SpA

- Alois Dallmayr KG

- Bewley's Limited

- J. J. Darboven GmbH & Co. KG

- Jab Holding Company

- Kruger Gmbh & Co. KG

- Luigi Lavazza SpA

- Melitta Group

- Tchibo GmbH

Frequently Asked Questions

Chapter 1 Scope of the Report

Chapter 2 Research Methodology

2.1.Research Process

2.2.Europe Coffee Market: Target Audience

2.3.Europe Coffee Market: Primary Research (As per Client Requirement)

2.4.Europe Coffee Market: Secondary Research

Chapter 3 Executive Summary

Chapter 4 Competitive Landscape

4.1. Europe Market Share Analysis, By Source, By Value, 2023-2030 (In %)

4.1.1.UK Market Share Analysis, By Source, By Value, 2023-2030 (In %)

4.1.2.France Market Share Analysis, By Source, By Value, 2023-2030 (In %)

4.1.3.Germany Market Share Analysis, By Source, By Value, 2023-2030 (In %)

4.1.4.Italy Market Share Analysis, By Source, By Value, 2023-2030 (In %)

4.1.5.Spain Market Share Analysis, By Source, By Value, 2023-2030 (In %)

4.1.6.Sweden Market Share Analysis, By Source, By Value, 2023-2030 (In %)

4.1.7.Austria Market Share Analysis, By Source, By Value, 2023-2030 (In %)

4.1.8.Rest of Europe Market Share Analysis, By Source, By Value, 2023-2030 (In %)

4.2. Europe Market Share Analysis, By Type, By Value, 2023-2030 (In %)

4.2.1.UK Market Share Analysis, By Type, By Value, 2023-2030 (In %)

4.2.2.France Market Share Analysis, By Type, By Value, 2023-2030 (In %)

4.2.3.Germany Market Share Analysis, By Type, By Value, 2023-2030 (In %)

4.2.4.Italy Market Share Analysis, By Type, By Value, 2023-2030 (In %)

4.2.5.Spain Market Share Analysis, By Type, By Value, 2023-2030 (In %)

4.2.6.Sweden Market Share Analysis, By Type, By Value, 2023-2030 (In %)

4.2.7.Austria Market Share Analysis, By Type, By Value, 2023-2030 (In %)

4.2.8.Rest of Europe Market Share Analysis, By Type, By Value, 2023-2030 (In %)

4.3. Europe Market Share Analysis, By Process, By Value, 2023-2030 (In %)

4.3.1.UK Market Share Analysis, By Process, By Value, 2023-2030 (In %)

4.3.2.France Market Share Analysis, By Process, By Value, 2023-2030 (In %)

4.3.3.Germany Market Share Analysis, By Process, By Value, 2023-2030 (In %)

4.3.4.Italy Market Share Analysis, By Process, By Value, 2023-2030 (In %)

4.3.5.Spain Market Share Analysis, By Process, By Value, 2023-2030 (In %)

4.3.6.Sweden Market Share Analysis, By Process, By Value, 2023-2030 (In %)

4.3.7.Austria Market Share Analysis, By Process, By Value, 2023-2030 (In %)

4.3.8.Rest of Europe Market Share Analysis, By Process, By Value, 2023-2030 (In %)

4.4. Stellar Competition matrix

4.4.1. Europe Stellar Competition Matrix

4.5. Key Players Benchmarking

4.5.1. Key Players Benchmarking by Source, Pricing, Market Share, Investments, Expansion Plans, Physical Presence and Presence in the Market.

4.6. Mergers and Acquisitions in Industry

4.6.1. M&A by Region, Value and Strategic Intent

4.7. Market Dynamics

4.7.1.Market Drivers

4.7.2.Market Restraints

4.7.3.Market Opportunities

4.7.4.Market Challenges

4.7.5.PESTLE Analysis

4.7.6.PORTERS Five Force Analysis

4.7.7.Value Chain Analysis

Chapter 5 Europe Coffee Market Segmentation: By Source

5.1. Europe Coffee Market, By Source, Overview/Analysis, 2023-2030

5.2. Europe Coffee Market, By Source, By Value, Market Share (%), 2023-2030 (USD Million)

5.3. Europe Coffee Market, By Source, By Value,

5.3.1.Arabica

5.3.2.Robusta

Chapter 6 Europe Coffee Market Segmentation: By Type

6.1. Europe Coffee Market, By Type, Overview/Analysis, 2023-2030

6.2. Europe Coffee Market Size, By Type, By Value, Market Share (%), 2023-2030 (USD Million)

6.3. Europe Coffee Market, By Type, By Value,

6.3.1.Instant Coffee

6.3.2.Ground Coffee

6.3.3.Whole Grain

6.3.4.Others

Chapter 7 Europe Coffee Market Segmentation: By Process

7.1. Europe Coffee Market, By Process, Overview/Analysis, 2023-2030

7.2. Europe Coffee Market Size, By Process, By Value, Market Share (%), 2023-2030 (USD Million)

7.3. Europe Coffee Market, By Process, By Value,

7.3.1.Caffeinated

7.3.2.Decaffeinated

Chapter 8 Europe Coffee Market Size By Country, By Value, 2023-2030 (USD Million)

8.1.1.UK

8.1.2.France

8.1.3.Germany

8.1.4.Italy

8.1.5.Spain

8.1.6.Sweden

8.1.7.Austria

8.1.8.Rest of Europe

Chapter 9 Company Profiles

9.1. Key Players

9.1.1. Nestle SA

9.1.1.1.Company Overview

9.1.1.2.Source Portfolio

9.1.1.3.Financial Overview

9.1.1.4.Business Strategy

9.1.1.5.Key Developments

9.1.2.The Kraft Heinz Company

9.1.3.Strauss Group Ltd

9.1.4.Melitta Group

9.1.5.Starbucks Corporation

9.1.6.Luigi Lavazza SpA

9.1.7.Alois Dallmayr KG

9.1.8.Bewley's Limited

9.1.9.J. J. Darboven GmbH & Co. KG

9.1.10.Jab Holding Company

9.1.11.Kruger Gmbh & Co. KG

9.1.12.Luigi Lavazza SpA

9.1.13.Melitta Group

9.1.14.Tchibo GmbH

9.2. Key Findings

9.3. Recommendations