Petrochemicals Market: Global Industry Analysis and Forecast (2024-2030)

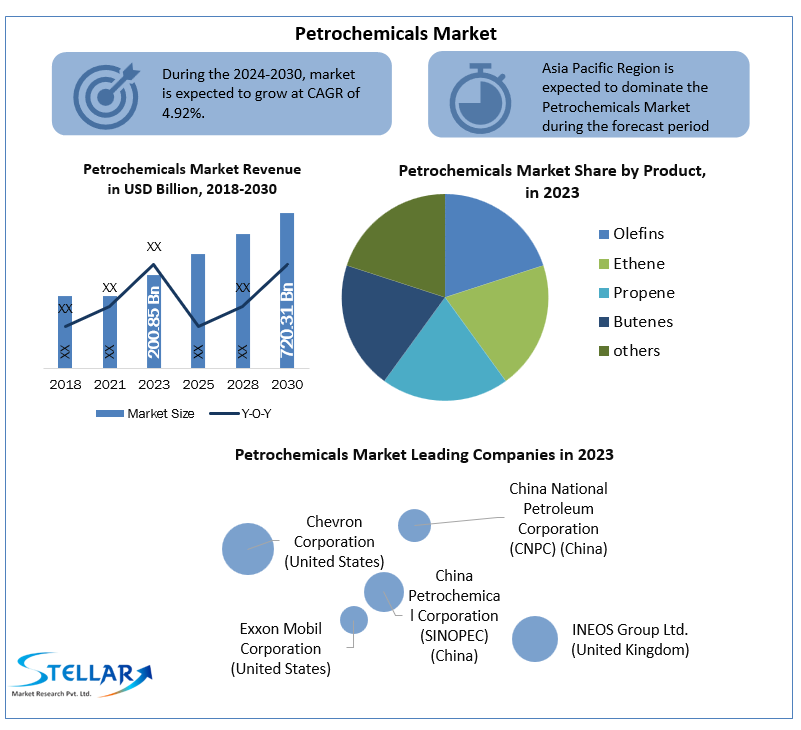

Petrochemicals Market size was valued at US $ 514.65 Billion in 2023 and the Petrochemicals market revenue is expected to grow at 4.92% through 2024 to 2030, reaching nearly US $ 720.31 Billion

Format : PDF | Report ID : SMR_290

Petrochemicals Market Overview:

Overall, petrochemicals market demand growth in 2020 was driven by rising demand for consumer staples such as household goods and personal products, as well as a decrease in demand for durables like automobiles and appliances. Volume rebounded in the second half of 2020 after the early shocks of the COVID-19 pandemic. As the price of oil fell, the worldwide ethylene cost curve flattened, decreasing feedstock advantages in places like North America and the Middle East. Also, project delays were frequent because of quarantine procedures and concerns about market uncertainty.

Supply and freight disruptions widened regional price disparities in the fourth quarter. North America, for example, experienced extra supply difficulties as a result of maintenance and unforeseen outages, resulting in price increases for Polyethylene (PE) and Polypropylene (PP). However, if the price of oil rises and the cost curve steepens, regional cost advantages may reap rewards. Similarly, volume growth rates are expected to return to expected levels based on historical trends, with less differentiation expected among chemical types and geographies. As expected, capacity comes online, low to medium use is expected in the olefins value chain. Global Petrochemicals market report is presented with the segment analysis, by type as Olefins and Aromatics along with region wise.

To get more Insights: Request Free Sample Report

Petrochemicals Market Dynamics:

Demand for essential hydrocarbons is driving the recovery:

During the third and fourth quarters of 2020, the chemical industry's revenues and earnings returned to pre-COVID-19 levels. Petrochemical businesses, for their part, continued to produce despite the economic crisis. For example, in 2020, one multinational chemical company with total assets of US $26 billion claimed a 1% increase in output volume over the previous year.

Brent crude prices fell from US $50 per barrel in the first quarter to US $30 per barrel in the second quarter, resulting in a significant drop in petrochemicals market revenue. As a result, petrochemical businesses' revenue fell sharply in the second quarter, before rebounding in the third and fourth quarters. In the second quarter, earnings before interest, taxes, depreciation, and amortization (EBITDA) fell across the board, owing to pandemic-related margin contraction and weaker demand.

Low oil prices, for example, caused the global cost curves for ethylene and PE to flatten in the second quarter. As a result, PE prices fell in lockstep with producers' marginal cash costs, and the lower oil-to-gas price ratio eliminated cost advantages in North America and the Middle East.

Petrochemical’s production to meet surging oil demand:

Chemicals demand for oil and gas is increasing at a rapid pace. This has always been the case, and expect it to remain so until 2030. Despite accounting for less than 15% of current oil consumption, the chemicals sector is expected to be the most important growth driver for global oil demand, accounting for four of the seven million barrels per day (MMb/d) increases between 2020 and 2030. Thanks to two key factors: First, an increase in the consumption of plastics in developing economies, resulting in a higher growth rate of petrochemicals market than GDP growth. Chemical demand continues to rise in developed economies as well but at a slower rate.

Second, other areas of oil and gas consumption are likely to expand at a slower pace, or possibly fall in some situations. For example, increased efficiency standards for internal combustion engines (ICE) and the uptake of electric vehicles (EVs) due to lowering battery costs are likely to lead worldwide oil demand for transportation to a peak before 2027.

Feedstock with a Limited Advantage:

In the petrochemicals market, conventional feedstocks have been used to produce petrochemicals and derivatives. North America and the Middle East (ME) have been the primary sources of these feedstocks in the sector thus far however, within the next five years, the potential for investments based on these traditional feedstocks are likely to be restricted. For example, in North America, the traditional feedstock is expected to diminish over the next ten years as export possibilities raise demand for ethane, among other things.

There are potential new sources of favorable gas supply across the world, as well as the likelihood of shale-gas extraction in nations like Argentina. Though, in comparison to what the Middle East and North America have delivered in the recent past, the number of possibilities, as well as their entry into markets, may be somewhat limited.

Crude Oil Price Volatility:

Since 2005, the price of crude oil, which is refined to generate benzene, ethylene, propylene, and other compounds, has risen steadily, peaking in 2008 at almost US $140 per barrel. Though, by 2014, prices had fallen from about USD 108 per barrel to under US $34 per barrel by January 2015, as non-OPEC oil production (especially in the United States) increased and global demand slowed. Also, the US Crude Oil First Purchase Price was $36.86 per barrel in January 2021, according to the US Energy Information Administration (EIA), compared to US $62.64 in August 2018 and US $55.65 in November 2018.

New Upstream Value-Creation Opportunities:

Many producers have all but severed the historic linkages between refining and petrochemicals as gas has become the preferred feedstock for petrochemicals. That could change: when options for chemical industries to employ gas feedstocks dwindle, they may turn to petroleum-based feedstocks once more. The appeal is likely to be mutual: oil corporations are fascinated by petrochemicals' stronger demand-growth potential when compared to fuel markets for heating and transportation. These fuel Petrochemicals Market

.s are likely to increase at a rate of less than 1% per year, but petrochemicals are expected to grow at a rate of 2 to 3% per year through 2030.

Petrochemicals Market Segment Analysis:

Based on Type: In 2023, the Aromatics segment was dominant and held xx% of the global petrochemicals market in terms of revenue. In Aromatics, ethylene was dominant. This can be related to its dominant consumption and an important source for plastics and industrial chemicals production globally.

Detailed information about each segment is also covered in the SMR’s report.

Petrochemicals Market Regional Insights:

In 2023, Asia Pacific dominated the petrochemicals market, accounting for more than 45% of the overall market share in terms of revenue. Increased domestic demand for petrochemicals as a result of the rapid growth of end-use industries is a key driver driving market growth in this region. To meet the increased demand for petrochemicals, companies in the region are turning to natural gas liquids and other non-oil feedstocks, as well as planning cost-effective ways to raise sales.

In 2020, North America had the second-largest revenue share in the petrochemicals market, and it is expected to grow at a CAGR of 6.62% over the forecast period. The ethylene segment in North America is expected to rise thanks to rising ethylene usage, particularly in anti-freezing/cooling applications in the automobile industry. Also, the packaged food industry's increasing use of ethylene is expected to contribute to its demand.

The objective of the report is to present a comprehensive analysis of the Petrochemicals Market to the stakeholders in the industry. The report provides trends that are most dominant in the Petrochemicals market and how these trends will influence new business investments and market development throughout the forecast period. The report also aids in the comprehension of the market dynamics and competitive structure of the market by analyzing market leaders, market followers, and regional players.

The qualitative and quantitative data provided in the Petrochemicals Market report is to help understand which market segments, regions are expected to grow at higher rates, factors affecting the market, and key opportunity areas, which will drive the industry and market growth through the forecast period. The report also includes the competitive landscape of key players in the industry along with their recent developments in the Petrochemicals Market. The report studies factors such as company size, market share, market growth, revenue, production volume, and profits of the key players in the market.

The report provides Porter's Five Force Model, which helps in designing the business strategies in the market. The report helps in identifying how many rivals are existing, who they are, and how their product quality is in the Market. The report also analyses if the Petrochemicals Market is easy for a new player to gain a foothold in the market, do they enter or exit the market regularly if the market is dominated by a few players, etc.

The report also includes a PESTEL Analysis, which aids in the development of company strategies. Political variables help in figuring out how much a government can influence the Market. Economic variables aid in the analysis of economic performance drivers that have an impact on the Market. Understanding the impact of the surrounding environment and the influence of environmental concerns on the Petrochemicals Market is aided by legal factors.

Petrochemicals Market Scope:

|

Petrochemicals Market |

|

|

Market Size in 2023 |

USD 490.52 Bn. |

|

Market Size in 2030 |

USD 686.54 Bn. |

|

CAGR (2024-2030) |

4% |

|

Historic Data |

2018-2022 |

|

Base Year |

2023 |

|

Forecast Period |

2024-2030 |

|

Segment Scope |

by Product

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Petrochemicals Market Key Players

- Chevron Corporation (United States)

- China National Petroleum Corporation (CNPC) (China)

- China Petrochemical Corporation (SINOPEC) (China)

- Exxon Mobil Corporation (United States)

- INEOS Group Ltd. (United Kingdom)

- Royal Dutch Shell (Netherlands)

- BP PLC (United Kingdom)

- Reliance Industries (India)

- Gazprom (Russia)

- Phillips 66 (United States)

- Rosneft (Russia)

- Equinor ASA (Norway)

- PJSC Lukoil (Russia)

- SABIC (Saudi Arabia)

- Abu Dhabi National Oil Company (ADNOC) (Abu Dhabi)

- Others

Frequently Asked Questions

The volatile prices of crude oil and feedstock with limited advantage are the key factors expected to hinder the growth of the market during the forecast period.

The Petrochemicals market is expected to grow at a CAGR of 4.92% during the forecast period (2024-2030).

The production of petrochemicals to meet growing oil demand globally is the factor expected to drive the growth of the market during the forecast period.

Chevron Corporation (United States), China National Petroleum Corporation (CNPC) (China), China Petrochemical Corporation (SINOPEC) (China), Exxon Mobil Corporation (United States), INEOS Group Ltd. (United Kingdom), Royal Dutch Shell (Netherlands), BP PLC (United Kingdom), Reliance Industries (India), Gazprom (Russia), Phillips 66 (United States), Rosneft (Russia), Equinor ASA (Norway), PJSC Lukoil (Russia), SABIC (Saudi Arabia), Abu Dhabi National Oil Company (ADNOC) (Abu Dhabi),& Others are the major key players covered.

Chapter 1 Scope of the Report

Chapter 2 Research Methodology

2.1. Research Process

2.2. Global Petrochemicals Market: Target Audience

2.3. Global Petrochemicals Market: Primary Research (As per Client Requirement)

2.4. Global Petrochemicals Market: Secondary Research

Chapter 3 Executive Summary

Chapter 4 Competitive Landscape

4.1. Market Share Analysis, By Value, 2023-2030

4.1.1. Market Share Analysis, By Region, By Value, 2023-2030 (In %)

4.1.1.1. North America Market Share Analysis, By Value, 2023-2030 (In %)

4.1.1.2. Europe Market Share Analysis, By Value, 2023-2030 (In %)

4.1.1.3. Asia Pacific Market Share Analysis, By Value, 2023-2030 (In %)

4.1.1.4. South America Market Share Analysis, By Value, 2023-2030 (In %)

4.1.1.5. Middle East and Africa Market Share Analysis, By Value, 2023-2030 (In %)

4.1.2. Market Share Analysis, By Type, By Value, 2023-2030 (In %)

4.1.2.1. North America Market Share Analysis, By Type, By Value, 2023-2030 (In %)

4.1.2.1.1. USA Market Share Analysis, By Type, By Value, 2023-2030 (In %)

4.1.2.1.2. Canada Market Share Analysis, By Type, By Value, 2023-2030 (In %)

4.1.2.1.3. Mexico Market Share Analysis, By Type, By Value, 2023-2030 (In %)

4.1.2.2. Europe Market Share Analysis, By Type, By Value, 2023-2030 (In %)

4.1.2.2.1. UK Market Share Analysis, By Type, By Value, 2023-2030 (In %)

4.1.2.2.2. France Market Share Analysis, By Type, By Value, 2023-2030 (In %)

4.1.2.2.3. Germany Market Share Analysis, By Type, By Value, 2023-2030 (In %)

4.1.2.2.4. Italy Market Share Analysis, By Type, By Value, 2023-2030 (In %)

4.1.2.2.5. Spain Market Share Analysis, By Type, By Value, 2023-2030 (In %)

4.1.2.2.6. Sweden Market Share Analysis, By Type, By Value, 2023-2030 (In %)

4.1.2.2.7. Austria Market Share Analysis, By Type, By Value, 2023-2030 (In %)

4.1.2.2.8. Rest of Europe Market Share Analysis, By Type, By Value, 2023-2030 (In %)

4.1.2.3. Asia Pacific Market Share Analysis, By Type, By Value, 2023-2030 (In %)

4.1.2.3.1. China Market Share Analysis, By Type, By Value, 2023-2030 (In %)

4.1.2.3.2. India Market Share Analysis, By Type, By Value, 2023-2030 (In %)

4.1.2.3.3. Japan Market Share Analysis, By Type, By Value, 2023-2030 (In %)

4.1.2.3.4. South Korea Market Share Analysis, By Type, By Value, 2023-2030 (In %)

4.1.2.3.5. Australia Market Share Analysis, By Type, By Value, 2023-2030 (In %)

4.1.2.3.6. ASEAN Market Share Analysis, By Type, By Value, 2023-2030 (In %)

4.1.2.3.7. Rest of APAC Market Share Analysis, By Type, By Value, 2023-2030 (In %)

4.1.2.4. South America Market Share Analysis, By Type, By Value, 2023-2030 (In %)

4.1.2.4.1. Brazil Market Share Analysis, By Type, By Value, 2023-2030 (In %)

4.1.2.4.2. Argentina Market Share Analysis, By Type, By Value, 2023-2030 (In %)

4.1.2.4.3. Rest of South America Market Share Analysis, By Type, By Value, 2023-2030 (In %)

4.1.2.5. Middle East and Africa Market Share Analysis, By Type, By Value, 2023-2030 (In %)

4.1.2.5.1. South Africa Market Share Analysis, By Type, By Value, 2023-2030 (In %)

4.1.2.5.2. GCC Market Share Analysis, By Type, By Value, 2023-2030 (In %)

4.1.2.5.3. Egypt Market Share Analysis, By Type, By Value, 2023-2030 (In %)

4.1.2.5.4. Nigeria Market Share Analysis, By Type, By Value, 2023-2030 (In %)

4.1.2.5.5. Rest of Middle East and Africa Market Share Analysis, By Type, By Value, 2023-2030 (In %)

4.2. Stellar Competition matrix

4.2.1. Global Stellar Competition Matrix

4.2.2. North America Stellar Competition Matrix

4.2.3. Europe Stellar Competition Matrix

4.2.4. Asia Pacific Stellar Competition Matrix

4.2.5. South America Stellar Competition Matrix

4.2.6. Middle East and Africa Stellar Competition Matrix

4.3. Key Players Benchmarking

4.3.1. Key Players Benchmarking by Type, Pricing, Market Share, Investments, Expansion Plans, Physical Presence and Presence in the Market.

4.4. Mergers and Acquisitions in Industry

4.4.1. M&A by Region, Value and Strategic Intent

4.5. Market Dynamics

4.5.1. Market Drivers

4.5.2. Market Restraints

4.5.3. Market Opportunities

4.5.4. Market Challenges

4.5.5. PESTLE Analysis

4.5.6. PORTERS Five Force Analysis

4.5.7. Value Chain Analysis

Chapter 5 Global Petrochemicals Market Segmentation: By Type

5.1. Global Petrochemicals Market, By Type, Overview/Analysis, 2023-2030

5.2. Global Petrochemicals Market, By Type, By Value, Market Share (%), 2023-2030 (USD Billion)

5.3. Global Petrochemicals Market, By Type, By Value, -

5.3.1. Olefins

5.3.1.1. Ethene

5.3.1.2. Propene

5.3.1.3. Butenes

5.3.1.4. Butadiene

5.3.2. Aromatics

5.3.2.1. Benzene

5.3.2.2. Toluene

5.3.2.3. Mixed Xylenes

Chapter 6 lobal Petrochemicals Market Segmentation: By Region

6.1. Global Petrochemicals Market, By Region – North America

6.1.1. North America Petrochemicals Market Size, By Type, By Value, 2023-2030 (USD Billion)

6.1.2. North America Petrochemicals Market Size, By Application, By Value, 2023-2030 (USD Billion)

6.1.3. By Country – U.S.

6.1.3.1. U.S. Petrochemicals Market Size, By Type, By Value, 2023-2030 (USD Billion)

6.1.3.2. U.S. Petrochemicals Market Size, By Application, By Value, 2023-2030 (USD Billion)

6.1.3.3. Canada Petrochemicals Market Size, By Value, 2023-2030 (USD Billion)

6.1.3.4. Mexico Petrochemicals Market Size, By Value, 2023-2030 (USD Billion)

6.2. Europe Petrochemicals Market Size, By Value, 2023-2030 (USD Billion)

6.2.1. UK

6.2.2. France

6.2.3. Germany

6.2.4. Italy

6.2.5. Spain

6.2.6. Sweden

6.2.7. Austria

6.2.8. Rest of Europe

6.3. Asia Pacific Petrochemicals Market Size, By Value, 2023-2030 (USD Billion)

6.3.1. China

6.3.2. India

6.3.3. Japan

6.3.4. South Korea

6.3.5. Australia

6.3.6. ASEAN

6.3.7. Rest of APAC

6.4. Middle East and Africa Petrochemicals Market Size, By Value, 2023-2030 (USD Billion)

6.4.1. South Africa

6.4.2. GCC

6.4.3. Egypt

6.4.4. Nigeria

6.4.5. Rest of Middle East and Africa

6.5. South America Petrochemicals Market Size, By Value, 2023-2030 (USD Billion)

6.5.1. Brazil

6.5.2. Argentina

6.5.3. Rest of South America

Chapter 7 Company Profiles

7.1. Key Players

7.1.1. Chevron Corporation (United States)

7.1.1.1. Company Overview

7.1.1.2. Type Portfolio

7.1.1.3. Financial Overview

7.1.1.4. Business Strategy

7.1.1.5. Key Developments

7.1.2. China National Petroleum Corporation (CNPC) (China)

7.1.3. China Petrochemical Corporation (SINOPEC) (China)

7.1.4. Exxon Mobil Corporation (United States)

7.1.5. INEOS Group Ltd. (United Kingdom)

7.1.6. Royal Dutch Shell (Netherlands)

7.1.7. BP PLC (United Kingdom)

7.1.8. Reliance Industries (India)

7.1.9. Gazprom (Russia)

7.1.10. Phillips 66 (United States)

7.1.11. Rosneft (Russia)

7.1.12. Equinor ASA (Norway)

7.1.13. PJSC Lukoil (Russia)

7.1.14. SABIC (Saudi Arabia)

7.1.15. Abu Dhabi National Oil Company (ADNOC) (Abu Dhabi)

7.1.16. Others

7.2. Key Findings

7.3. Recommendations